Optimal Blue Summit 2026 LIVE BLOG – State of Mortgage Markets & Fintech

Welcome The Basis Point Live Blog of Optimal Blue Summit 2026. Optimal Blue is one of the largest fintech firms in the mortgage sector, and the category leader in software that powers how lenders manage the quantitative process of doing mortgages — from first quoting rates to consumers all the way through secondary market trading.

Loan pricing, product eligibility, hedging, and trading functions are the lifeblood of the mortgage industry, which will fund $2.2 trillion in new loans in 2026, and service $14.9 trillion in outstanding loans this year.

These mortgage industry stats are simply huge, and Optimal Blue prices and locks 35% of these fundings, and supports 70% of the valuations on mortgage servicing rights (MSRs).

As The Basis Point’s Optimal Blue Summit 2026 Live Blog kicks off below, I cover more of these stats to get you acclimated. Then the Live Blog will cover sessions, themes, quotes, and fun stuff from the show at Talking Stick resort in Scottsdale.

The event has 500+ attendees this year. This is about double last year’s size, and includes most major mortgage lenders, servicers, other fintechs, investors, GSEs, mortgage insurers, and other major players in the space.

This Live Blog done in real-time, so if you see anything that needs adjusting — or if you have questions — please reach out.

___

I want to thank Optimal Blue for letting The Basis Point cover their flagship client conference in real time. The views, thoughts, and opinions expressed here are solely those of The Basis Point and do not necessarily reflect the official policy or position of Optimal Blue, LLC, its affiliates, or any other individuals or entities associated with Optimal Blue, LLC.

Optimal Blue Summit 2026 Live Blog Table Of Contents

- Optimal Blue Takeover at Talking Stick Resort & Casino In Scottsdale

- Even The Room Keys Are Branded Optimal Blue

- My Own History On Optimal Blue

- Some Key Facts & Stats About Optimal Blue

- Optimal Blue Summit 2026 Main Room Filling Up Before CEO Joe Tyrrell Kicks Off

- What’s Coming In Mortgage Tech – part 1

- What’s Coming In Mortgage Tech – part 2

- What’s Coming In Mortgage Tech – part 3

- What’s Coming In Mortgage Tech – part 4

- What’s Coming In Mortgage Tech – part 5

- Optimal Blue Summit 2026 Exhibit Hall

- Optimal Blue Virtual Economist – part 1

- Optimal Blue Virtual Economist – part 2

- Capital Markets Innovation In Non-QM Lending – part 1

- Capital Markets Innovation In Non-QM Lending – part 2

- MBA Economic Outlook with Mike Fratantoni – part 1

- MBA Economic Outlook with Mike Fratantoni – part 2

- MBA Economic Outlook with Mike Fratantoni – part 3

- MBA Economic Outlook with Mike Fratantoni – part 4

- MBA Industry & Reg Outlook with Bob Broeksmit – part 1

- MBA Industry & Reg Outlook with Bob Broeksmit – part 2

- Growing Profitability In High-Cost Mortgage Market – part 1

- Growing Profitability In High-Cost Mortgage Market – part 2

- Growing Profitability In High-Cost Mortgage Market – part 3

- Turning Rate Sheets Into Competitive Advantage

- Turning Rate Sheets Into Competitive Advantage – part 2

- Optimal Blue Machine Learning

- Optimal Blue Machine Learning – part 2

- Optimal Blue Machine Learning – part 3

- A Word On The Importance Of Networking (and shout to Optimal Blue for helping)

- Sun & Strategy Rising Over Optimal Blue Summit 2026

- Quick Rundown Of Optimal Blue’s Formidable Partner Network (and partner leader Chazz Huston)

- Investor Perspectives On Markets & Trading

- Investor Perspectives On Markets & Trading – part 2

- Investor Perspectives On Markets & Trading – part 3

- Optimal Blue CMO Sara Holtz Shouts Out The Basis Point Live Blog

- Executive Lender Outlook 2026 & Beyond

- Executive Lender Outlook 2026 & Beyond – part 2

- Executive Lender Outlook 2026 & Beyond – part 3

- Executive Lender Outlook 2026 & Beyond – part 4

- Olympian Michael Phelps with OB CEO Joe Tyrrell

- Olympian Michael Phelps with OB CEO Joe Tyrrell – part 2

- Olympian Michael Phelps with OB CEO Joe Tyrrell – part 3

- Olympian Michael Phelps with OB CEO Joe Tyrrell – part 4

- Meta Live Blog Shout Out Being Live Blogged, LOL

- Final Thoughts On Products, Leadership, Culture Of Optimal Blue Circa 2026

Optimal Blue Takeover at Talking Stick Resort & Casino In Scottsdale

Love this ceiling signage as you walk into the resort in Scottsdale.

Even The Room Keys Are Branded Optimal Blue

The Optimal Blue marketing and events team has every detail covered for the Summit.

Here are some shots from arriving and the opening party and overall setting from last night.

Really wonderful setting for networking and talking mortgage strategy.

My Own History On Optimal Blue

Optimal Blue was founded in 2002, and when I entered the mortgage industry as a loan agent in 2003, I didn’t have it yet, but after I saw it, I was one of the loan agents demanding it from my mortgage bank.

When we finally got it a couple years later, it was indispensable because you no longer had to search every different lender’s rate sheet to find the best price and most relevant for a customer.

A lot has changed since then because product and pricing engines (PPEs) were not always as reliable as they are today on products.

It was all about the price, but you could quote a price only to find out later that the product didn’t work for that customer. Today, Optimal Blue has been the leader on helping loan officers vet loan approval guidelines at the same time as they’re quoting the price.

Not only that, but they also now do near-miss scenarios. This means that if your borrower’s down payment or credit score or deb-to-income ratio is slightly off, OB will show you what’s close.

This makes loan officers smarter and faster at advising their customers.

The other thing I appreciated about OB as I grew into managing large teams of loan officers is the ability to manage the financials of your branches and regions.

You can set different company margins at the product level (e.g., Confirming Fixed, Conforming ARM, FHA, VA, USDA, Jumbo, Non-QM, HELOC, etc.), which not only makes loan officers more competitive, but it also helps lenders focus on what they specialize in, and not miss a beat on financial management.

And this is to say nothing of all the secondary market functionality, which will be covered later in the Live Blog.

But for now, it’s worth noting that when I said in a post above that “this is the life blood of the mortgage industry,” it’s not an exaggeration.

This is how you price deals to earn and win business from every customer, everyday. And it’s how you manage your business too.

Some Key Facts & Stats About Optimal Blue

Optimal Blue was acquired by a company called Black Knight July 27, 2020, and while Black Knight was more known for mortgage servicing software, they understood the power of Optimal Blue.

It contributed to Black Knight being a priority acquisition target of Intercontinental Exchange (ICE), and in September 2023, ICE paid $12 billion for Black Knight, America’s largest mortgage servicing software and mortgage data firm, which included Optimal Blue.

Previously, in September 2020, ICE had paid $11 billion for Ellie Mae, America’s largest mortgage originations software firm, and they had appointed Ellie Mae COO Joe Tyrrell as president of the entire ICE Mortgage Technology operation.

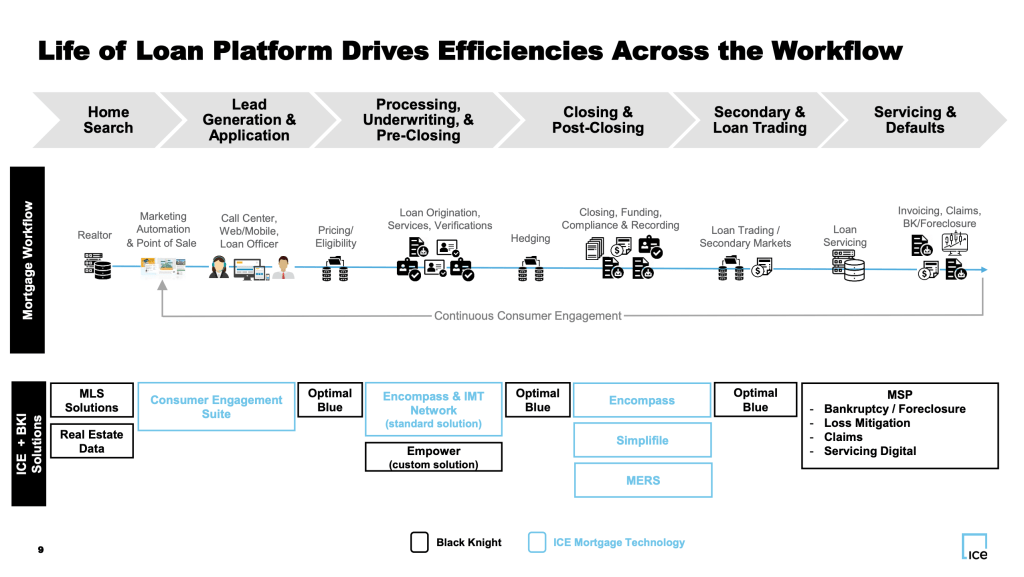

After ICE bought Black Knight, I always appreciated how they positioned Optimal Blue as critical to the entire loan process. Below is a slide from their investor materials showing how important Optimal Blue is in the process.

Fast forward through the ICE dealmaking, their priority was to focus on their main origination and servicing software platforms.

Optimal Blue was spun out of ICE, making it an independent service provider to the entire industry, and a product, pricing, and secondary market fintech partner for ALL systems, not just ICE.

This has meant that Optimal Blue is one of the most interoperable systems in all of mortgage. It’s integrated into most loan origination, servicing, marketing, point of sale, and other loan systems in the industry.

And in June 2024, Joe Tyrrell became CEO of Optimal Blue.

I remember thinking “wow, perfect fit” when I saw that news.

Why? Because Joe is an ecosystem company leader — having led ICE into mainstream mortgage software leadership — and Optimal Blue is an ecosystem company itself.

In the past year, he’s made Erin Wester head of product and Mike Vough head of strategy to expand Optimal Blue’s capabilities and dealmaking.

More to come on that as the Optimal Blue 2026 Live Blog continues.

In the meantime, here are a few key stats about the breadth of Optimal Blue.

OPTIMAL BLUE BY THE NUMBERS

– 65% of the top 500 lenders are customers

– 60% of the top 50 lenders are customers

– OB prices and locks 35% of mortgages completed in America

– OB supports 40% of loans hedged and sold into the mortgage secondary market

– OB supports 70% of MSR valuations done in the mortgage industry

– OB supports 255 million rate searches annually

– OB supports 135k users, 3500 lenders, and 260 investors

Optimal Blue Summit 2026 Main Room Filling Up Before CEO Joe Tyrrell Kicks Off

The not-so-quiet before the Live Blogging gets underway.

Most folks are still at breakfast, but starting to come into the main room for keynote kickoff by CEO Joe Tyrrell…

What’s Coming In Mortgage Tech – part 1

Optimal Blue Summit 2026 Live Blog 2026 kicks off with CEO Joe Tyrell saying 23% of people quit New Year’s resolutions by January 9.

It’s called quitting day. And Joe asks why change is so hard.

The trans theoretical model of change says that contemplation, prep, action all have to come before actually maintaining a routine.

And without consequences, people and companies won’t change.

The main consequences in our industry has been regulations.

Now another key consequence is AI.

It’s not going to replace jobs as much as some worry.

But there will be consequences from falling behind — the biggest of which is lower profitability.

What’s Coming In Mortgage Tech – part 2

Joe Tyrrell CEO keynote continues with Roger’s adoption model, which is summarized in the 2 images below.

The second image above looks exactly like the Transtheoretical Model of behavioral change.

You need to face consequences in order to make change.

In mortgage, if we don’t help people get into homes, there are consequences for them and for us.

That’s the best motivation possible to do the best we can to help at all times.

How do we get to Yes responsibly?

AI will help humans help other humans in a few ways.

First, we must take control by adopting AI to help us, not replace us.

Second, don’t algorithm the human value of the expertise you bring. AI is great at summarizing data, but less strong so far at making decisions on that data. That is still the job of humans, especially in mortgage which is so highly regulated and markets are so volatile.

Also human judgment is required for individual company risk tolerances. So AI gathers and summarizes the data, and human expertise is making decisions using this data.

Third, aim for the best Yes possible, not the fastest No.

Mortgage isn’t a black box, it’s a thousand black boxes of loan guidelines, prices, and regs. You can use AI to organize all of this. Then you can make decisions to help more borrowers.

KEY EXAMPLE:

Near-miss scenarios provided by Optimal Blue AI give loan teams the scenarios that a borrower might be close to if they can work with their lender to make slight adjustments to their down payment, credit, DTI, etc.

This is the difference between closing and not closing, and the difference between being able to say yes and no to a borrower.

What’s Coming In Mortgage Tech – part 3

Optimal Blue CEO Joe Tyrrell said the only thing worse than a bad process is a bad process that’s automated.

That’s why OB end-to-end data is so important so when you apply AI, everything is precise.

Chief Marketing Officer Sara Holtz previewed some of the Summit’s key agenda items on OB feature like virtual economist technology, daily AI-generated profitability analysis for capital markets desks.

And also a preview of MBA market outlook (coming on the Live Blog).

Now Erin Wester, chief product officer, to run down some new products.

She continued where Joe left off by saying how OB is about getting to best possible Yes for borrowers and it’s about helping capital markets teams run their day to day simply.

One key are here is AI to answer questions cap markets teams people have every day.

These questions include:

====

QUESTIONS CAP MARKETS PROS ASK OPTIMAL BLUE AI

How much was my average margin percent by loan type for august 2025?

Who are my top 5 originators in lock volume in the past 2 years?

Year to date production by Loan officer

Identify the top MSA with the highest margins for Q3 2025

average 30 year fixed note rate for loans locked since september

What is the percentage of refinance transaction vs. purchase transactions?

Which branch issued the most concessions this year?

Provide YTD avg markup percentage

Can you break down my loans by investor for the last 3 months?

What are the top 5 markup levels which have the highest average margin % last month?

compare my average markup from august to september

How much revenue did we receive on FHA loans through markups in March?

What originator locked the most loans in the past 6 months?

how many 30 year commitments with fannie mae do i currently have

how many 5/1 arm locks last week

What branch originated the most loans year to date?

in the last month how do my rates compare to peers in my MSAs

who are my top 15 originators in lock volume in the past 1 year?

What loan types are included in Expanded Guidelines?

What is the percentage of locks this year by product type?

List each individual loan locked in 2025, include Base Price

Excluding extensions and rate relocks, how many change requests were submitted for the Wholesale TPO channel last month?

====

This is a huge deal … instant answers to these questions are critical to managing lender operations precisely and profitably.

What’s Coming In Mortgage Tech – part 4

Chief Product Officer Erin Wester runs down a key new products, starting with Virtual Economist.

Kevin Foley on her team previewed Virtual Economist, and how it moves at the speed of the market.

Example: maintenance, explainability, interactivity are all absent from today’s forecasting tools.

Virtual Economist is like talking to your company’s chief economist about rates and volume whenever you want.

Foley did a live demo with a live video avatar of your ‘economist’ and began with today’s Optimal Blue rate index level.

…Which by the way is 5.94%!

Rates below 6%, yay!

Then the demo provided a rate forecast of rates for 2026. It uses predictions on 10yr note, primary and secondary spreads, and MBS spreads, plus analysis of key economic indicators.

Foley noted you can also ask the Virtual Economist about Fed cut projections.

There’s another session later today that I’ll Live Blog on this topic.

What’s Coming In Mortgage Tech – part 5

Erin then previewed the Profitability Center, which connects pricing, hedging, and AI-powered market and economic intel.

The Ask Obi AI module is at top of the UX, so you can ask it the questions like I noted in part 3 above.

This used to mean stitching many systems and spreadsheets together, now it’s one consolidated view of how lender profitability is created and maintained.

Everything is summarized and also down to the loan level.

Also compares company lock volume vs. industry averages so you can see how you compare.

===

Next is a preview of hedging relative to rate locks by integrating pricing and hedging platforms.

This lets capital markets teams view and approve post-lock decisions in real-time.

KEY:

Rate sheet competitive analysis in real-time BEFORE releasing rate sheets.

This enables lenders to ensure they’re competitive relative to anonymous broad market data.

===

As for administration, the product and pricing engine (PPE) UX is revised to show a lender all their channels (retail, wholesale, direct, etc.), all product types, regions, loan guidelines, etc. so lenders can do all their pricing in one place consistently.

And now they can use AI rules assistant to create pricing rules based on criteria above, so they can more efficiently manage PPE parameters ongoing.

===

Agency Direct lets lenders capture required basis points and model forward commitments all in one place.

===

In CompassEdge hedging and trading platform, lenders can also now directly connect with Tradeweb for real-time connectivity to replace manual execution on TBA trades.

This is powering $571b in trades now (and growing), which saves 55 workdays per year.

===

Loansifter and Comergence integration is for lenders who serve the broker community, and enables them to be just as efficient with broker pricing as they are with retail.

NOTE: I’ll add more to the Optimal Blue 2026

Live Blog on these products later. This segment was a rapid-fire introductory summary.

Optimal Blue Summit 2026 Exhibit Hall

There are about 40 exhibitors and sponsors in the Optimal Blue Summit 2026 Exhibit Hall, which proves an earlier point I made in the Live Blog about how many companies integrate with the Optimal Blue ecosystem.

Also, what you can’t see in the photos is how truly central all the exhibitors are. This is key because the networking area, the session area, and the exhibitor area are all one single location.

So you have to pass the exhibitors to get to sessions and find people for side meetings.

This is so key for all attendees of conferences, and helps everyone be productive.

Optimal Blue Virtual Economist – part 1

Optimal Blue Live Blog 2026 continues with a deeper dive on Virtual Economist which I introduced in the last session.

Below is the core methodology behind building this AI avatar economist any lender can talk to just like they would a human economist in their shop.

In their 10 year Note model, the inputs include:

-GDP growth

-Fed funds rate

-VIX volatility

-10yr break even inflation expectations

-(plus 5 other factors)

For MBS spread they look at things like:

-MBA purchase and refi app indices

-MOVE options volatility

For Primary Secondary Spread, they look at:

-2yr/10yr spread

-MBs current coupon

-Proprietary lock volume

-Proprietary margin

-Volatility

For lock volume forecasting they look at:

-OB rate index

-Seasonality

All of this comprises methodology for rate outlook coming out of the AI Virtual Economist.

For accuracy on 10yr note model, they’re looking for R-squared of 0.4 to 0.8, and generally hit .53, which is above 0.1 to 0.3 for other common forecasting methods.

For MAPE (where lower is better), they’re at 2.8% vs. over 3% for other common methods.

For MBS spreads, primary-secondary spreads, and lock volume, they outperform common benchmarks similarly.

Optimal Blue Virtual Economist – part 2

As I noted in the original preview notes do Virtual Economist, the Virtual Economist UX is super clean.

For competitive reasons, I can’t show screenshots, but picture a human avatar on screen next to a Claude/OpenAi-like chat interface, and you can chat with the avatar or type in your questions.

What will rates do this month and year?

Could you provide the baseline lock volume for each month in 2026 compared to last year?

The latency is minimal … what you’d expect from a consumer-grade voice and chat AI agent — which is basically a few seconds.

By the way, the answer to that last question about lock volumes is that rate locks generally rise as we move through 2026.

When you ask about whether a new Fed chair would cut rates as expected, here’s what you get:

It models out rates based on whether the Fed cuts by 1.5% more than expected.

By the way, most of those monthly scenarios put monthly rates slightly below 6%.

Kevin asked why rates wouldn’t be lower than this (which I would have raised my hand and asked if he didn’t) and the answer explained that the 10yr note and MBS might not respond as much to Fed cuts. It also offers to explore how different assumptions about inflation, growth, or market uncertainty might affect the rate forecast.

I felt like that was pretty smart, and in the same spirit as the best consumer AI, it engages with you like a human — but it doesn’t hallucinate.

===

Next question: what is lock volume if the Fed cuts 1.375% more than expected.

It performed similarly as above, which is to say: it performs like a human economist would with cautious if/then scenarios.

===

Kevin fielded a question about whether they model in Fed asset purchases and sales, and they do.

They’re going to publish a white paper with all methodology soon.

===

Main Takeaway 1: this is a killer tool deploying in April, and it’s important to know that it’s calibrated to give feedback and analysis just like a human analyst would, thereby enabling capital markets teams to assess its output and make decisions based on their risk philosophy and approach.

Main Takeaway 2: I think this would also be killer for consumer-facing loan teams to get market intel — especially when they work for smaller companies that don’t have cap markets or economist teams that are big enough to serve all the loan teams with daily market intel questions. It’s not meant for that yet, but with the proper guardrails, it’s another key use case.

Capital Markets Innovation In Non-QM Lending – part 1

Non-agency and Non-QM loans are differentiated by loan size and qualification.

DSCR, Bank Statement, and Jumbo loans are the 3 main categories Optimal Blue watches.

Private label securities make up about 7% of the market.

So there’s been growth with Non-QM, but still a lot of room for growth.

Mike Vough with OB and Geoffrey Sharp with Eris Innovations say that the Non-QM has opened up because we need more buyers of loans than just GSEs (and before that, banks).

Sharp says it might cap out at 15% of the market, but it could be more if there are proper guidelines and rules.

John Coleman at RJO (a StoneX company) noted that guidelines and rules are solid now. Higher credit scores in 700+ range and lower LTVs.

Non-QM is performing better than segments of agency loans, like FHA/VA.

KEY Coleman note: today’s non-QM is NOT subprime. It’s fundamentally different, and originators are acting very responsibly about underwriting.

Vough said underwriting quality mostly comes down to how Non-QM loan types are qualified.

EXAMPLE:

DSCR needs rent to cover the debt obligations. If rents drop, then there’s a risk. But it’s worth noting (by The Basis Point, not the speakers) that DSCR has grown as rents have been dropping. This implies lenders are practicing proper discipline on conservative DSCR ratios. If these ratios were to allow less padding for rents to drop (and allowable LTVs go too high), then both lender and systemic risk can arise.

However, the Non-QM investor market would just stop buying loans and/or stop allowing loose guidelines if loan performance dropped out due to market factors like plummeting rents.

Capital Markets Innovation In Non-QM Lending – part 2

As for borrower rates and investor yields, Non-QM is affordable for borrowers who don’t otherwise qualify for traditional W2 style underwriting while providing higher yields for investors.

Agency loan pricing is driven by different factors than non-agency, not the least of which is repeated use of quantitative easing by the Fed and now the GSEs at the behest of the White House.

But for Non-QM, SOFR rate is something of a North Star for pricing, and independent mortgage banks can now access the same level of Non-QM hedging and trading sophistication as Wall Street banks thanks to Optimal Blue.

OB helps teams more precisely manage interest rate sensitivity of these loans.

Sharp on risk management: You boil your risk down into components you can hedge. For example: what dollar price change do I have per basis point change in SOFR rates? I can hedge this with TBAs against SOFR.

===

Coleman on hedging: the value of an asset is present value of future cash flows. In a drug analogy, if you buy a kilo of something, carve it into smaller pieces and sell those, it’s worth more than the kilo. That same concept applies to mortgage trading.

===

With OB for Non-QM, the PPE tracks locked loans and reports daily.

There’s noise on this pricing because of things like prepayment penalties.

The OAS is the price we need to get to for profitability, so OB regression analysis tells us what rates best achieve OAS goals.

The whole goal of hedging is offsetting potential losses in one position with gains in another.

Without OB, Non-QM teams are doing some of this in spreadsheets or other systems. But because OB has both the PPE where the loans are locked (along with all loan-level price adjustments, including LLPAs for prepays, etc.), and the hedging and trading where you manage profitability using the PPE data, you can be far more precise and efficient.

One key note here: you wouldn’t typically use the OBMMI rate do do this, you can instead use SOFR or something more aligned with Non-QM market.

===

EDITOR NOTE: this session was technical, but in the spirit of the Live Blog, I try to assimilate the trader language into plain English in real time, so for readers I hope this makes sense. And for traders, if I oversimplified any of this, please ping me and let me know.

MBA Economic Outlook with Mike Fratantoni – part 1

Mike started the outlook with some volatility caveats. Tariff uncertainty, war in Iran, election year are 3 examples.

Unemployment rate holding low, but new graduates are having trouble getting jobs.

Hiring rate remains low, quit rate declining.

Uneven growth in payrolls across the country.

Also, consumers struggling with debt. 90-day lates on student debt spiked to 9.36%.

Projection for unemployment rate at 4.5%, which is steady, but inflation for now is heading the wrong way as measured by PCE.

This has a lot to do with tariffs. Starting 2025, tariffs were 2.5%, then we got to mid teens. SCOTUS decision would have cut this in half, but new White House tariff approach brings it back to mid teens.

RATE OUTLOOK

25 basis points of additional cuts from Fed, and steeper yield curve.

This despite White House pressure. Warsh won’t replace Powell until Cook DOJ investigation is revolved. Tillis on Senate Banking committee has vowed this.

Warsh is 1 of 12 FOMC votes so the 25 basis point cut (vs. ostensibly more based on White House goal) feels justified.

MBA Economic Outlook with Mike Fratantoni – part 2

As for refis, it’s short bursts as rates dip then rise again.

We end February with rates just below 6%.

GOOD NEWS: If rates drop 0.5% from here, almost all production since 2022 is refinancable.

As for home buying, purchase applications pacing above 2025.

Inventory increasing meaningfully above pre-pandemic levels in South and West.

Home prices are dropping in increasing number of metros. Builders continue to offer incentives.

Most major home price projections for 2026 are close to flat.

EDITOR NOTE: This is a good thing because it’s more affordable for buyers without a crash for sellers.

FHA share of loans nearly 20%, which has helped a lot of people get into homes.

But delinquency rates on FHA loans are now above 11%.

As for refis, a lot more people are going into ARM loans.

MBA Economic Outlook with Mike Fratantoni – part 3

Outlook for mortgage volume is $2.2 trillion, up 8% — see below.

And total units predicted to be 5.8 million, up 7% — see below.

And if rates were higher or lower by 100 basis points, the third image below shows how much the outlooks would change.

===

Bank pull through is 55%, and no bank is 69%.

This means a LOT of work is being done on loans that don’t close.

Really need to solve this.

EDITOR NOTE: Tech people always say tech is the way to solve it. But it’s not just tech. And it’s not just sales folks who can’t close. It’s also a more fickle consumer led more easily astray by online shopping culture.

===

4.45% unemployment rate tracking very closely to 4.26% delinquency rate for all loans.

But FHA loan delinquency rate is 11.52%. This is something to watch closely.

Tightening of forbearance and other pandemic relief rules is a big contributor here.

It costs servicers about $1700+ per loan to handle loans with hardships vs. about $180 for performing loans.

MBA Economic Outlook with Mike Fratantoni – part 4

As for lenders retaining loans, we’re up to 20% retention of both purchase and refi loans — image below.

EDITOR NOTE: This could go higher when trigger lead ban goes into effect in March.

Why? Because servicers who already have the loan will face less competition picking those customers off once they run credit for a refi.

Therefore I think we could hit retention rates well above 20%.

MBA Industry & Reg Outlook with Bob Broeksmit – part 1

Sarah Wheeler asked MBA chief Bob Broeksmit what are the biggest issues right now.

Two things he started with. First, trigger lead ban that MBA helped get done will help lenders retain more loans.

Second, smaller lenders get worried about competition from big players consolidating, but Bob believes this won’t be an issue. Smaller lenders are nimble, and can compete.

I would add that with parity on the fintech that’s available, smaller players can offer the same consumer and loan officer experience as big players.

“There’s plenty of room for everybody” in an industry with $2.2 trillion in annual fundings.

===

As for GSE reform, the real issue is whether or not they’re released from conservatorship after 18 years.

This has to be done very carefully. You can’t put in jeopardy the 30-year fixed loan with no prepayment penalty and steady rates across full market cycles.

MBA met with Treasury chief Bessent last week who agrees with this sentiment, and understands that you can’t rush this — plus there’s no reason to rush it in an election year after a successful run of 18 years.

MBA Industry & Reg Outlook with Bob Broeksmit – part 2

MBA got everything it wanted out of Big Beautiful Bill including trigger lead ban and helping veteran borrowers get partial claims.

The VA partial claim means that these borrowers can pause payments when in hardship and the unpaid part gets added to the loan. This keeps veterans in their homes.

===

Bob’s advice to White House on housing.

MBA has been pushing 4 ways to help housing affordability, first noted in a letter to Hassett.

– Ban of Institutional homebuyers and properly defining these buyers as owning 100 units or more.

– Lower loan level price adjustments for Fannie Mae and Freddie Mac loans.

– Lower FHA mortgage insurance premiums because the FHA fund is properly funded now. Even with delinquencies rising, the fund could still handle a 2008 like crisis.

– Modernize credit reporting requirements to save borrowers about $300 per loan. Lenders have to build credit report costs for unclosed loans into their financial projections — and only 55% of bank loans and 69% of nonbank loans close right now.

===

More details on credit reporting modernization:

3.3 years ago FHFA said a 3-bureau credit run dint have to happen on every loan, but we’re still doing it, and it’s more expensive for lenders and consumers.

Normally lenders use the middle of the 3 scores. There’s a debate over whether this is helpful for loan safety, and the debate is legit.

Reform suggestion: Lenders can still pull 3 scores, but if they had an option to just pull one, they should be able to. But if they pulled 3 voluntarily, they have to submit it.

FHFA director Pulte could allow this with the stroke of a pen. He’s expressed interest, but hasn’t don’t it yet.

===

Will banks get back into mortgage origination and servicing if bank capital rules are relaxed?

Yes, absolutely.

Everybody wins if banks do this. It’s more competition for mortgage servicing rights, and this benefits consumers and lenders of all sizes.

Growing Profitability In High-Cost Mortgage Market – part 1

Stratmor senior partner Garth Graham kicks off with why U.S. railroad gauge is 4’ 8.5”, and the answer is that’s what British tools existed when they came and started building roads. And this dates back to Ancient Rome for horse carriages.

The punchline: all roads are the width of 2 horses’ asses.

The point: you can’t always blindly rely on yesterday’s tools.

===

Refi typically up or down at least 20% every year.

Purchase units have been flat from 2024 to 2028 (projected).

===

About 2 of 3 refi units are done by call centers, vs. 1 in 5 for purchase units.

This means we haven’t cracked the code on purchases in consumer direct, but definitely consumer direct dominates refis.

===

58% of bank and credit union home equity loans aren’t sourced in branch.

Then there’s the new trend that Figure validated:

They charge way more for home equity (higher margins above Prime), but they’re incredibly fast. And they’ve proven that borrowers will pay more if they get their equity now.

Growing Profitability In High-Cost Mortgage Market – part 2

The percentage of profitable nonbank mortgage lenders aka Independent Mortgage Banks (IMBs) is growing. See chart. But it’s only $853 per loan, which isn’t profitable enough.

KEY POINT: we’re making money now not because of cutting costs but because of growing revenue.

But there’s progress. Fulfillment employee productivity has risen 30% from 2022 to 205.

But overall for all production employees, they’re still only handing 1.5 loans per employee.

===

What’s the impact of consolidation?

Normally when profitability goes up, number of M&A deals goes down.

But that’s not happening now. See chart.

There are now more deals even as profits are rising.

Why? Because Rocket buying Mr. Cooper created some pressure to get bigger to get better warehouse lines and pricing. And some believe this pressure will continue for the bottom third of lenders.

===

Loan officers doing at least 10 units has dropped to 92,000.

Top 30% of loan officers do 80% of the loans.

===

Average expenses remain high over the past 5 years.

In retail (left chart), half the cost is sales.

Also note the tech cost is relatively low.

Growing Profitability In High-Cost Mortgage Market – part 3

Banks spend more on tech than IMBs, seen in this chart.

But IMBs spend less on people, seen in this chart below. Which means IMBs are getting more out of their tech.

And here’s what lenders tell Stratmor they think of the tech that they use today.

===

WHAT ANNOYS CUSTOMERS THE MOST

– Repeat questions

– Apply online (especially after talking to someone already)

===

The “Why” Of Getting A Mortgage

Every loan application conversation should seek understand the why.

This is the thing tech cannot do.

And if you do, then the tech can help you package rate and fee quotes. But the why is where you give them advice, and this is what they remember.

It’s the difference between consumers feeling SOLD TO rather than SERVED … and PARTNERED WITH rather than PROCESSED.

As for retention being at just 20% (see MBA section of Optimal Blue Summit 2026 Live Blog), this is the reason. And if you change this, your retention rates will rise.

Turning Rate Sheets Into Competitive Advantage

Optimal Blue Summit 2026 Live Blog continues with an overview of how lenders can determine whether their rates are competitive.

Patrick and Kevin will run down front-end product and pricing engine (PPE), rate sheet generation options, PPE and hedging system integration to ensure consistency, and some AI tools across the board.

RATE SHEET GOAL: you need to be able to create rate sheets with 15, 30, 45, 60, and 90 day locks that are competitive for loan officers and their consumers while providing estimated future sell pricing for all these terms — this is the key to profitability.

One key use case Optimal Blue helps you address in realtime: MBS market has sold off 8 ticks (fyi a tick is 1/32 which is 3.125 basis points) and 2 of 4 investors has repriced for the worse. You can get a realtime view of this and determine if other adjustments are needed before potentially out of market locks come in.

Related: the bulk mark to market pricing in the Compass Edge hedging system lets you reconcile with rate sheets in real time as well.

Also in the Compass Edge rate sheet tool, you have key features like setting exception tolerances and rate differentials for investor changes.

This is all enabled by realtime data connection between Compass Edge hedging system and PPE.

Turning Rate Sheets Into Competitive Advantage – part 2

New rate sheet base price configuration enables investor toggle on and off with intraday market movement.

===

HOW COMPETITIVE IS PRICING RELATIVE TO PEERS?

After I build my rate sheets, I can use anonymous OB data to see industry average rates by region or loan type or loan purpose.

The reason this matters is because it combines PPE pricing, hedging and trading assumptions, and then brings in industry average data so you can see exactly how your price compares.

For example, if you’re in the 78th percentile and you need to be in the 95th percentile for that product or loan purpose, you can make those adjustments.

===

As for AI, you can query anything you’re working on in natural language — including the example above where you’re comparing pricing to anonymous national averages — and Ask Obi AI will summarize findings for you right in the Compass Edge interface.

EDITOR NOTE: I’ve hosted a couple public demos with Optimal Blue since they deployed Ask Obi last year, and the AI is really powerful. In the What’s Coming segment in Live Blog Table of Contents above, you can see a list of highly granular questions that cap markets desks are asking, and getting granular answers based on their PPE and hedging/trading data (as well as the anonymized industry benchmark data).

Optimal Blue Machine Learning

The Optimal Blue Summit 2026 Live Blog continues with advances in machine learning which I’m excited about in the context of a company like this with so much data.

Kevin said machine learning is mainly about statistical analysis.

Gen AI models are to create by producing text, images, audio, etc in a non-deterministic way.

ML is about predicting or classifying for a specific purpose, and its deterministic. Like a google search.

Every day uses:

How many locks should I expect next week?

Did today’s rate locks deviate from normal patterns?

What’s the probability this rate lock will fall out?

===

This is why the ML model is so important to OB strategy.

They use public data (MBA, Fed, etc.), proprietary data, anonymized client data (rates, pull through, etc.).

The ML lifecycle at OB is framing problem, get/explore/prepare data, train/fine tune models, deploy models, monitor/maintain models.

Optimal Blue Machine Learning – part 2

The types of ML models OB looks at are:

– Linear regression: High explainability, lower performance.

– Non-linear regression: less explainable, higher performance.

– Time based: seasonality and time based factors.

– Forecasting and predictive: extrapolating current trends vs. predictive inputs

They choose from the models above based on the project. Then they test accuracy with:

– Coefficient of determination: R-squared

– Mean absolute percentage error: MAPE

This is a more detailed description of how the Optimal Blue AI Virtual Economist (see Virtual

Economist section above in Live Blog Table of Contents) functions.

In that section, I covered how accurate OB’s AI economist tool is compared to industry benchmarks.

Spoiler alert: the R-squared and MAPE scores for the main models that go into the Virtual Economist (like 10yr Note outlook, MBS spreads, primary/secondary spreads, and broader economic indicators) are scoring more accurate than other widely accepted scoring models.

EDITOR NOTE: I strongly suggest reading the Virtual Economist section of the Live Blog (see Table of Contents – link below) to see how this machine learning methodology has created a killer AI product.

Optimal Blue Machine Learning – part 3

Next up for Virtual Economist is modeling scenarios in graph form.

For example you can chart rate lock projections based on rates being 100 basis points higher or lower than baseline estimate.

They’ll also add originations forecasting, MBS issuance, prepayment modeling.

It’s also worth noting that as lenders in the room wrap their heads around this capability, they’ll keep pushing new ideas.

I noted in Live Blog above that I loved the idea of letting loan officers have the Virtual Economist to help address daily rate projection questions they get from clients.

Kevin brought that up in this ML session, and it was met with both excitement and a bit of cringing from lenders who know that there’s some risk to letting LOs quote a Virtual Economist when fielding customer inquiries.

But I maintain, that with the right guardrails that this is an exciting use case that LOs would welcome.

And seeing how good the Virtual Economist is today — plus the discipline with which OB is training it, I think we’re not far from enabling a use case like this for LOs.

A Word On The Importance Of Networking (and shout to Optimal Blue for helping)

What an amazing sunset party. The past 2-3 hours just flew by … great low key but deliberately planned networking setting.

Again, huge props to Sara, Caryn, Olivia, Matt, Mike, Erin, Chazz, and the whole Optimal Blue team for providing such a conducive environment for lenders, investors, fintechs, policy pros, and so many other industry participants to collaborate and find ways to work together.

As I’ve said in this Live Blog, Optimal Blue has grown into an ecosystem company because it is such critical operational infrastructure from Main Street lenders to Wall Street traders.

And it’s also because they position themselves to be the center of so much high quality relationship management and development. That’s the human side of it that’s hard to capture until you come participate in an event like Optimal Blue Summit.

Here are some pics of the setting tonight. Spread out, tons of food, cool DJ — this could have gone all night.

Sun & Strategy Rising Over Optimal Blue Summit 2026

I talked last night about the networking environment being very conducive to relationship building.

This morning I’ll add that the overall setting in Scottsdale is conducive to strategic thinking.

Here’s a shot of the setting to get the day started here in Scottsdale, and on the Optimal Blue Summit 2026 Live Blog.

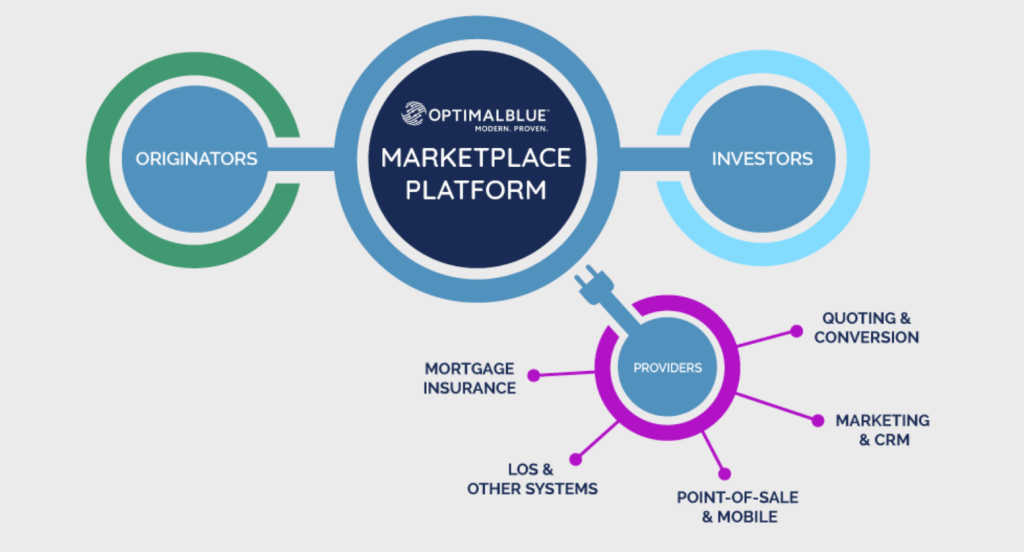

Quick Rundown Of Optimal Blue’s Formidable Partner Network (and partner leader Chazz Huston)

I want to give a special shout out to Chazz Huston who runs partnerships at Optimal Blue.

This Live Blog has talked about the depth of OB integrations across the tech ecosystem, and here are some details.

Optimal Blue’s partner network is 70+ integration partners that use their open APIs to create custom UX on their side.

A few examples include:

– Online rate quoting: lenders use OB integrations to feed pricing into their UX that’s quoting rates to consumers.

– CRM & marketing systems: lender CRMs use OB integrations to run real-time rate/product scenarios against all existing borrower profiles to offer deals proactively that might benefit borrowers.

– Consumer-direct websites: If you’re seeking rates from lenders online, there’s a good chance the lender you’re seeing rates from is feeding in rates from Optimal Blue.

– Mobile originator solutions: There are many systems loan officers use like point of sale systems to take loan apps (or let borrowers complete loan apps), to processing tools that help get borrowers approved. All of these systems also integrate with OB to provide loan programs and rates as part of that process.

– LOS and other systems of record: Optimal Blue is rarely called a system of record because Loan Origination Systems are the lenders’ systems of record, but OB is definitely a sub system of record that provides loan programs and pricing into the LOS systems. OB is first quote to consumer through loans closing and the cap markets trade, and by definition, this must be integrated tightly into the systems of record.

– Mortgage Insurance: Again, mortgage insurance integrations are a must rather than optional because they’re a feature of the loan program for LTVs higher than 80%, so this is another integration that’s essential to lender ops.

– Hedging: And of course if you don’t use OB for hedging (which they have), you can integrate OB PPE into your hedging platform.

For all of these, you can see here which integrations are live in each of these categories.

Props to Chazz, who’s got a huge job keeping this ecosystem thriving. Plus he’s just a great guy. Earnest to the last, and a fellow fan of outdoor sports 🙂

Investor Perspectives On Markets & Trading

This session is with Fannie and Freddie plus 2 lenders/investors: Newrez and Plaza Home Mortgage.

Rebecca at Newrez announced the a new integration to make secondary trading one step. This is a big development and it’s no additional cost from OB perspective.

James with OB talked about Non-QM locks growing to 10% of overall lock volume.

They’ve also been starting to hedge. He asked Rebecca to comment on why today’s Non-QM is different than Alt-A or Subprime of previous eras.

Rebecca said this comparison is a mistake. We’re verifying income and ability to repay (which wasn’t happening in previous era), and it’s serving borrowers who are eligible — just not in a traditional W2 earning sense.

Example of where Non-QM works well: a former exec who retired and tried to buy a second home, and despite having 8-figures in the bank, they couldn’t qualify on traditional loans.

Another example: if you use a CPA to verify your bank statement income, we can do those loans.

Example 3: DSCR loans at Newrez will allow down to 0.5% ratio — maybe lowest in industry now — but they’ll require larger down payments and credit score to offset this.

Every investor will allow non-delegated underwriting for Non-QM so as an originator, you have low risk if you want to get into this segment.

EDITOR NOTE: Non-delegated underwriting is good for originator risk management, but it’s less control at the retail loan officer level because you’re handing the process and timing over to the investor.

Investor Perspectives On Markets & Trading – part 2

As for counting non-liquidated crypto as assets to qualify for Non-QM, Newrez is the fist to allow this.

They manage for the volatility by pricing for the risk. So it’s more for the borrower but the tradeoff is worth it for those borrowers.

Also Rebecca made a note about non-warrantable condos being something they are comfortable with from a risk standpoint.

EDITOR NOTE: I have a long history of condo lending and love hearing that Newrez gets non-warrantable condos. This doesn’t mean they just take undue risk on lending for units in condo projects. It means that they get that if there’s something like non-structural litigation in a project, or if a newly built project hasn’t met traditional Fannie/Freddie presale requirements yet, it’s still worth lending on. We need investors who get this, and props to Newrez for understanding and supporting this part of the market.

===

On affordable housing, the GSE goals will still support first time homebuyers.

Lower rates have helped — rates are down from 7.25% a year ago, and are now at 6%.

This is significantly better than it’s been.

This is helping refis for now.

But it’s too early to see whether we’re going to get an uptick in Spring homebuying.

MBA and Fannie Mae both project rates will remain around 6% for 2026 because of tariff and other market uncertainty that could be inflationary.

Investor Perspectives On Markets & Trading – part 3

ARM loan trends are growing, but banks and credit unions have been dominant because they can leave these loans on their balance sheets.

When they don’t sell, they don’t have secondary cost, which means they can price ARMs lower for consumers. That’s why they can perform better than originators selling to investors.

Fannie Mae is seeing $625k average ARM loan amount.

ARM advantage for borrowers is obviously the lower payment relative to higher-rate fixed loans.

Freddie Mac said they’re also seeing more interest in ARMs.

Both agencies are supporting SOFR for the ARM index.

KEY: Some investors will use CMT as an index, but these loans aren’t eligible for sale to the GSEs.

===

Quantitative easing via $200b GSE purchases of MBS — will this continue?

The GSE answers to this was: we’re getting the policy tweets at the same time as everyone else.

EDITOR NOTE: I took this to mean there’s no plans for more QE unless it comes from the White House.

Optimal Blue CMO Sara Holtz Shouts Out The Basis Point Live Blog

Meta moment. Getting ready for the next session on executive outlook, and OB CMO Sara Holtz reminded everyone that the Live Blog is a good way to catch up on anything people missed. Honored to be doing this!

Sara also teased next year’s Summit is in Scottsdale again on February 1-3.

Executive Lender Outlook 2026 & Beyond

Maria at Lennar said scale lenders aren’t the competitive market share killers some fear them to be. We all have the same tools so smaller players can compete just as well with the big firms.

As for margin compression, Mike at OB said we don’t even really know what normal margins look like after tough years.

Kevin at PRMG said that margin and yield have been greatly helped by newer products like Non-QM.

He also shouted out 5-handle on rates as a ray of hope for affordability. Amen to that.

Kevin does believe we’ll have consolidation among IMBs because of margin compression and technology efficiency.

Example: his firm decided to spend $14m on tech in 2026 before they funded their first loan for the year.

Boomer widows is an emerging market. This was half a joke, but it’s true. They can tap equity to fund retirement, elder care, or helping younger family members get down payment.

Executive Lender Outlook 2026 & Beyond – part 2

Maria at Lennar said rate volatility is permanent. You must understand this, and you must be diversified in your warehouse liquidity resources so you can withstand rate shocks.

Kevin at PRMG said he’s surprised at bearishness of market outlooks, and while he gets it, he’s also more optimistic.

He said it’s possible we’re at bottom of rate cycle, which would reconcile with MBA, Fannie Mae, and other outlooks.

Ken at PRMI said rates weren’t enough to change their ops overall. Lower rates make homes more affordable. But more inventory would help more. He believes low rates we had before and during pandemic are NOT realistic.

When we had 3% rates, home prices spiked, and this isn’t sustainable. Now builders are key to helping solve affordability.

Maria agrees with this from her builder perspective. She said even when they incentivize borrowers with extremely low rates, even that isn’t enough.

Executive Lender Outlook 2026 & Beyond – part 3

Spring purchase season will be an important test of consumer sentiment. We have rates 1.25% lower than last year, and this season will show us if that helps.

As for mortgage technology, Kevin noted that there’s some who have a vision of letting borrowers control the whole process. But he respectfully asks: Do they really, though?

EDITOR NOTE: I agree with this sentiment. Consumers need help. And if that help also includes each lender giving them the tech needs to get a loan done, then so be it. Plus, lenders are too highly regulated than to just accept and be compliant with borrower controlled tech for them providing all that’s needed to document a loan to get approved.

Example: Maria said she at first thought AI underwriting would lead the way, but she said she was wrong because, while the tools are interesting, they can’t do what humans need to do to get loans approved.

But she DOES believe that arming sales teams (loan officers and production teams) with the best lender-approved tech is a priority and is good for lenders and consumers they serve.

Ken said AI can make loan officers more productive — like with Allregs or other loan guideline research tools to find the right deals for customers — but it also risks making loan officers lazy, and removing their ability to be experts.

EDITOR NOTE: this is a delicate balance, because lenders could employ less experienced loan teams

for less, but are they actually learning, or just relying on AI to think for them. A more existential question, but a very real issue in this era.

Executive Lender Outlook 2026 & Beyond – part 4

Maria said she is a big fan of AI’s ability to look at large sets of data and assimilate it to help her team make decisions faster.

She mentioned being wowed by the insights Claude can produce with their data, so her teams can make decisions. She said it would take an analyst in her world days to do this kind of insight the Claude can do almost instantly — IF the data going into the AI is good. So getting clean data is now a key priority.

Kevin said one of the biggest issues we can solve as an industry is shortening the time it takes to settle a security. This is helped by end-to-end systems like Optimal Blue, but market structure can only reduce it so much.

EDITOR NOTE: Is blockchain the answer? I would like to hear Mike and OB sound off on this topic. The Basis Point will be doing some follow up podcasts with Optimal Blue after this Summit, so I’ll ask him when we do that.

===

On Gen AI, Maria said their priorities are coming bottom up rather than top down. The teams on the ground are finding interesting use cases, and Lennar culture allows this.

Ken said there’s a lot of experimentation, but adoption is low/inconsistent (I appreciate the honesty here).

Kevin said again that sales teams are a great way to test and get adoption of AI. But also he noted that sales teams have to get good at this because their consumer customers are also good at — and actively using AI.

Olympian Michael Phelps with OB CEO Joe Tyrrell

Joe kicked off with the Olympics having just ended and that medal moment being so special — but until you get to talk to 28 medal winner (including 23 golds and 38 world records) Michael Phelps, you don’t know what goes into getting to that medal moment. Now this session will run it down.

Facing top athletes in the world over 5 Olympics, what separates you?

My career started when my mom put is in the water for water safety.

I got into the water and was afraid to put my face in the water. So I learned backstroke first.

I met my coach at 11 playing baseball and he said I could be an Olympian in 4 years, which I did make the team at 15.

I did it because someone believed in me.

The feeling of defeat in that first Olympics (didn’t medal by 32/100 of 1 second) was the primary motivating factor.

Six months after that I broke my first world record.

Going into 2004, all I wanted was 1 gold medal, and I got 6. I won Butterfly by 4/100 of 1 second.

In 2008, I won one of the medals by 1/100 of 1 second.

I once was asked by a journalist if I felt bad winning so many medals. What??!! Not at all. I worked harder.

For everyday you’re out of the pool, it takes 2 days to get back up to speed.

I would work out about 30 hours a week, but all the rest and recovery exercises, eating right (10k calories per day) to maintain 5% body fat at 185 points all takes the rest of the day.

We used to stroke in time 50s to test lactic acid an endurance, which is why we were better.

My first goal I ever wrote was to “Win a gold Metal” and I was 11.

EDITOR NOTE: this metal head loves the inadvertent metal reference 🤘🏻

Olympian Michael Phelps with OB CEO Joe Tyrrell – part 2

Phelps believes the reason he performed on the biggest stages with the brightest lights is because he prepared.

Visualized, practiced, exhausted every scenario before he went live so when he did he was chilled out.

After 2008 success, the period going into the 2012 Olympics was the worst prep period of my career. It was because I was being a kid.

Then after that by 2014, I really was in a dark place wondering if I wanted to live.

I had never done the personal work of being a person rather than an Olympian machine. I dealt with my depression and anxiety and this climb to 2016 was one of the most positive experience of my life.

By then I had a 3 year old son and I was 32 competing against kids who were my age when I started. And in some ways I was a dad to them.

And being able to be my own authentic self in this era for the first time has been the best experience of my life.

If you come to a dead end on something you want to do, just find a way with this:

Dream. Plan. Reach.

Then if you get tripped up, you revert to previous step.

Olympian Michael Phelps with OB CEO Joe Tyrrell – part 3

It takes 30 days to form — and to break — a habit.

Most people forget this.

Every time I show up for a workout, I’m making a deposit into the bank.

If I just show up no matter what, if I’m sore or tired, it’s a deposit. Don’t miss a step.

And if you do, then you revert to Dream, Plan, Reach sequence — and again, you revert to the previous step if it’s not working.

VISUALIZATION

Physical, mental, emotional preparation are ALL required.

You must create a voice in your head to keep telling yourself so you can get there.

You also must give your body and your mind what they need to be your authentic self. We all have the talents to achieve what we want if we can visualize and then prepare.

===

What is your foundation?

I got a $1m bonus in 2008 for winning 8 gold medals.

Water safety is how my mom started me, and that was the start of the foundation. But also because of my depression and anxiety, we added a mental health component.

So we incorporate this into helping people overcome their fears. The stories that come out of seeing how kids overcome this is life changing.

We’ve taught just over 40k kids, and I’ll be doing this until the day that I die.

Olympian Michael Phelps with OB CEO Joe Tyrrell – part 4

Do you let your kids win at board games, etc.?

Hell no. My competitiveness just takes over.

When I was going through goal setting with my coach at age 11, he taught me to remove the word “can’t” from my vocabulary.

Even if I can’t do something today, removing this word from my vocabulary just means I need to show up, so well and figure it out.

Form habits over 30 days, then 60, 90, 120 and then you realize there’s nothing you can’t do.

We are who we are in any moment and the things we can control are controllable.

There is so much that’s out of our control, but NEVER lose sight of what we can control.

EDITOR NOTE: The things we can control are controllable. I wanted to repeat that quote from Phelps because it’s so much deeper than it seems on the surface. Something I’ll be thinking about for a long time until it becomes second nature to see the world and my goals this way.

Last note from Phelps: if you see someone who’s struggling, check in on them. Those little things matter more than you can imagine. Just ask if they’re ok. For them to feel seen is everything.

He does this with a core group of men including The Rock, and they look out for each other this way.

===

What a great session. Phelps was so open and unafraid to express some vulnerability.

Meta Live Blog Shout Out Being Live Blogged, LOL

This is a funny double meta photo of Optimal Blue CMO Sara Holtz telling attendees who missed certain sessions to check out The Basis Point Optimal Blue Live Blog, and a picture of me blogging it live.

Photo credit: OB partnership lead Chazz Huston. Don’t miss the post above about everything Chazz does to built the tech integration and real-life Optimal Blue partner community consisting of more than 70 companies.

Final Thoughts On Products, Leadership, Culture Of Optimal Blue Circa 2026

As I said when the Optimal Blue Summit 2026 Live Blog began, OB CEO Joe Tyrrell is a veteran leader of scale ecosystem companies. Previously he ran ICE Mortgage Technology, today’s largest fintech firm in our sector.

And if there’s one takeaway from this OB Summit, it’s that the OB executive team and all of their respective teams are fully empowered to own their purviews and push forward for customers and the industry.

I can smell manufactured company culture a mile away, and Optimal Blue on Joe’s watch is anything but that. Teams are passionate, and it’s because they have freedom to build and innovate. A proper CEO can enable this at companies of this scale, but no CEO can manufacture it.

That’s why I don’t think it’s a coincidence that OB has been cranking out new products and iterating on (as well as integrating) their entire end-to-end suite from product and pricing engine all the way through capital markets — and doing so while getting to a single dataset, which is the key to success for implementing AI use cases.

To be real, OB was not this fast or precise for a while before Joe and his current management team took over. The lending community would express big ecosystem company gripes. Stuff like: “they’re important but innovation is slow.”

But today’s OB is nothing like that. The product is tight from end-to-end, and the iteration energy — and ability/drive to execute — is real. That’s being driven by execs like product head Erin Wester, strategy head Mike Vough, and technology head Seever Sulaiman, as well as so many other strong managers and committed teams.

That’s why marketing chief Sara Holtz told me it was so important to rebrand the company.

Key to that rebranding is today’s tagline:

Optimal Blue

Modern. Proven.

I had seen this when the team first rolled it out (long before this Summit), and spent some time wondering if the tagline should maybe focus on lender profitability.

But in studying the company closely for the first time in awhile while doing this Live Blog, I’ve seen the ‘lender profitability’ message fully permeated in company positioning.

And after seeing how customers are receiving this hard-charging provider of core industry infrastructure (remember I noted earlier that these products are lifeblood for lenders), it’s sunk in for me why the “Modern. Proven.” tagline is a bullseye for this era of Optimal Blue.

Bravo to Joe for his transformative leadership, and to the team for showing customers how serious you are about what matters most to them.

And special shouts to Olivia DeLancey, Caryn Wiggins, and Matt Gilhooly, and the entire OB marketing team for flawless scale event execution — and thanks for allowing The Basis Point to actively participate.

This concludes the Optimal Blue Summit 2026 Live Blog on The Basis Point.

See you next time. 🫡