MBA Annual 2024 LIVE BLOG – State of Mortgage Markets, Rates, Regs, Lenders

Hey folks, here’s The Basis Point Live Blog for MBA Annual 2024 from Denver.

This is the largest and most influential mortgage industry conference each year.

Stay tuned October 27-29 as we update all things mortgage originations, servicing, affordability, rates, regs, tech, and lender health after 2+ tough years in housing.

This year, there are almost 4000 attendees, and the energy is palpably higher than the last 2 years.

Below you’ll get all the latest from regulators, lenders, servicers, plus both Wall Street and Main Street perspectives on the housing economy.

We go very fast on this stuff to because it’s truly live, so if your organization is discussed below and you see something is off, please reach out.

And of course please reach out with questions. Some of this stuff is wonkier than our normal analysis and commentary.

MBA Annual 2024 Table Of Contents

- The quiet before the blogging storm

- Mortgage Market Outlook – MBA economists Mike Fratantoni & Marina Walsh, part 1

- Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 2

- Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 3

- Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 4

- Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 5

- Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 6

- LOL SNL Weekend Update parody to kick off MBA Annual 2024

- Denver Mayor Mike Johnston on how Denver is doing, and buying his own house this week

- New MBA chair Laura Escobar on 3 top priorities for MBA & U.S. housing

- MBA CEO Bob Broeksmit With MBA Annual 2024 and 2025 Priorities

- Mohamed El-Erian on economy, rates, election

- Mohamed El-Erian on markets, economy, election, Part 2

- Mohamed El-Erian on markets, economy, election, Part 3

- State of Mortgage Tech 2025 & 16 Demo Demo Showcase – MBA Annual 2024

- Vesta

- Candor Technology

- SimplyIOA

- IDIQ

- Mortgage365

- LenderLogix

- Xactus

- Calyx Path

- How To Reform 50 Year Old Real Estate Referral Regulations (RESPA)

- Friendlier Consumer Appraisal & Lender Buyback Policies From Fannie & Freddie Regulator FHFA

- The Promise & Possibility of AI

- MBA Annual State of Mortgage Tech & Demo Showcase – Day 2 (AI Focus)

- LoanPASS

- Friday Harbor

- Insellerate

- Sagent

- Jaro

- Blend

- OptimalBlue

- Ocrolus

- Is Mortgage Bear Market Finally Over In 2025? (MBA Annual 2024 recap)

The quiet before the blogging storm

Getting started soon…

Mortgage Market Outlook – MBA economists Mike Fratantoni & Marina Walsh, part 1

Markets are betting on a red wave in U.S. election, which is days away.

With either administration, direction of monetary policy is easing.

MBA thinks Fed Funds Rate gets cut to 3.5% and not lower.

CPI and PCE as well as Core numbers ex food and energy are all near Fed targets.

But Fed won’t go too far to re-ignite inflation.

Job market is still very strong. Unemployment 4.1%

But people more cautious about moving jobs.

Households still borrowing but facing strain.

HELOC delinquencies low but auto and credit card balances AND delinquencies are both higher than just a year ago.

KEY: Mortgage delinquencies and unemployment rates track closely.

4.5-4.7% is MBA unemployment projection and this means mortgage delinquencies could rise similarly.

Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 2

Debt to GDP is too high and a huge problem.

Here’s a chart of whole history of this ratio.

We don’t think rates are much below 6.0% next year.

White 72% vs. black 45% homeownership rates are drastically too disparate.

As for mortgage volume, we should end at $1.8t

Next year is $2.3t.

Very solid increase.

See chart.

Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 3

Housing inventory tight but growing. See 2 images below for details.

Under building has contributed to lower supply.

Applications to buy homes — purchase applications — are especially for newly built homes.

See chart below.

FHA share of purchase applications is growing. Now at 28.7%.

This is a strong indicator of first time buyers being active (since FHA loans are largely to first timers).

Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 4

Average loan size for refis is $340,800, and this is down recently but generally has been growing.

It’s easier for people with bigger loans to refi.

It’s easier for folks to cover refi fees with bigger loans.

Home price appreciation moderating from a spike of 18% in 2020-21.

But now we’re at 3.8% and lower in next couple years.

If true this may control affordability in next cycle.

But NOT prices dropping.

See chart for forecast.

Property taxes and insurance are hitting borrowers hard. See charts for dollar and percent increases.

Mortgage units to grow 28% in 2025.

Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 5

As for lender profitability, lenders had first profitable quarter in 2 years for 2Q24

Profitability for 2Q is up 17 basis points after 8 quarters of negative basis points.

Marina thinks 3Q could look similar to 2Q because loan costs were down $1800 per loan on the quarter.

These figures are profit excluding servicing.

Costs to do a loan in a bank is $17k+.

For a nonbank the cost is $13k+.

See 2 pie charts below for details on core costs.

Note that what these don’t include is tech costs.

In the MBA dataset that covers this (Performance Report), tech costs are around 3-4% of this per loan cost total for nonbank.

Also note the pull-through rates below pie charts. A lot of work for loans that aren’t closing.

Recent improvement in productivity is key.

See chart below. But also: 1.4 closed loans per full time sales/fulfillment employee?!

Can’t we do better than that as an industry?

I’ll be addressing this in my State of Mortgage Tech demo segments. Tech has to help more here.

Is product differentiation an advantage.

Marina says below are the differentiators lenders say they’re having success with.

Mortgage Market Outlook – MBA economists Mike Fratantoni, Marina Walsh, Joel Kan part 6

Household delinquencies are higher.

FHA at 10.6% with forbearances at 4 straight months.

Total equity $35.1 trillion and total debt $14.1 trillion.

This means the U.S. has a 29% loan to value ratio.

This is incredibly healthy.

As for scenarios on how rates will impact overall mortgage market activity, the charts below show what would happen if:

– Rates are 100 basis points higher

– Rates are 100 basis points lower

Great session as always from Mike, Joel, Marina.

So grateful to have them keeping a close eye on the numbers.

LOL SNL Weekend Update parody to kick off MBA Annual 2024

This was a killer segment, and legitimately funny. Bravo MBA team showing your comedy chops.

Denver Mayor Mike Johnston on how Denver is doing, and buying his own house this week

Denver mayor Mike Johnston is closing on a house this week!

Johnston talked about their efforts to help the homeless.

They have spent the last year moving 2000+ unhoused into housing.

They’re the first to end veteran homelessness.

They’re making development easier by making new building projects easier to approve at the city and for builders to make money.

Quick remarks but really cool to see him come out.

New MBA chair Laura Escobar on 3 top priorities for MBA & U.S. housing

Laura made some opening remarks about her new role as MBA chair.

I don’t want to only give speeches.

I want to be in the crowd learning.

I want to be in front of lawmakers and regulators collaborating.

We need to bring all the intensity we can muster to solve housing supply, affordability, and education.

These are the 3 biggest issues facing America’s housing market.

Housing supply is about not just building new homes.

It’s about rehabbing existing homes.

Burdensome local regs make this too difficult.

75% of land in U.S. is zoned single family. Need more multifamily.

$390k to build a home. This is too high.

MBA needs to lead this fight.

Supply AND demand solution: the top way to solve affordability is to build more homes.

In addition to supply, there are other ways to solve for affordability.

Insurance and taxes are up 52% and 19% since 2019.

It costs more than $11k for a lender to do a loan.

In 2022 alone, loan costs rose $2k.

My message to every policymaker is:

Stop talking about affordability. Demonstrate it.

As for education, we need to invest more than ever educating our mortgage pros and bringing in more young and diverse people.

One reason I was a top loan producer is because I spoke Spanish.

We’ve started doing mortgage banking curriculum at 2 universities, and we’ve got certificate programs in the works with at least 4 others.

This is the site for education initiatives:

As for activity in Washington, MBA is recognized and respected by both parties.

This is something we’ll stay committed to.

MBA CEO Bob Broeksmit With MBA Annual 2024 and 2025 Priorities

MBA CEO Bob Broeksmit kicked off with an emotional tribute to Dave Stevens who made MBA a force for consumer advocacy in housing.

Dave was a mentor to me and collaborator who passed after a battle with cancer this year and I want to thank Bob for keeping Dave’s legacy front and center.

He also talked about how one of Dave’s key legacies is working with both parties in Washington.

Bob talked about how election outcomes are really tough.

Mortgage rates around 6% to 6.5% through 2024 and high 5s by late 2025.

Trump and Harris will look vastly different and MBA will keep its consumer housing focus regardless of who’s in White House.

Doing so is also a path to still navigate House and Senate even if there’s gridlock.

As for Basel III, we worked with Fed, congress, White House, OCC, and FDIC to help them understand how these proposed rules would adversely hit low to mid income consumers.

This led to a reworking of Basel III which were still involved with.

As for trigger leads, we helped create Homebuyer Privacy Act to get even the most fiercely partisan lawmakers from both sides of the aisle are jointly aligned on.

This will help protect consumers from endless calls when their credit is run.

Both Harris and Trump prioritize lower costs for homebuyers and renters.

We’ll be working with both of them.

As for the tax debate, we’ll keep pushing for consumers to take home more of their pay.

MBA will also be pushing for a national housing director to corral all the different housing regulators and GSE initiatives.

We’re working with both campaigns to help push this and all other housing policy initiatives above.

We went to both conventions with full teams to work on these relationships.

We met with at least 20 senators at Trump convention.

Then at Harris convention, we did a meeting with the senator leading tax policy. We told them Harris tax policy was more about demand than housing supply.

The outcome was that, even though Democrats aren’t supply siders in broader economic policy. But now they are supply siders when it comes to housing.

I (Julian) believe supply sider philosophy when it comes to housing — this is a key topic The Basis Point will cover more.

Mohamed El-Erian on economy, rates, election

Mohamed El-Erian is former PIMCO CEO, president of Queens College, University of Cambridge. Now he’s chair of Gramercy Fund Management, and a contributor to Bloomberg and FT.

This is a broad segment on market and election topics.

The economy has a 70% of doing better than today.

The other 30% is recession risk.

The lower end of incomes are more in trouble. Will this spread? That’s what we’re watching closely.

Other recession risks are geopolitical and domestic policy.

But for now, we’ve got a very exceptional economy.

MBA chef economist Mike Fratantoni asked if U.S. is still cleanest dirty shirt in global economy like El-Erian has said before.

He said yes. We’ve got too much debt, flip flopping Fed, etc. But we’re better than other super powers.

Watching Fed policy should be like watching paint dry.

It should be less exciting than it is. And it is because the Fed’s data dependency makes them change their views a lot.

So the market has to keep recalibrating.

Right now Fed Funds Rate is 5% and he thinks it’ll be 3.5%. And he hopes this is slow, steady 25 basis point cuts instead of flip flopping.

Is the direction of travel or pace of cuts more important?

Pace is key.

Going 50 basis points then zero then 50, etc. this creates volatility.

Forward policy guidance is supposed to reduce volatility.

But for now it’s worse.

However they’re trying to correct it by replacing “data dependent” with “forward looking guidance.”

It’s like being in a plane with a pilot over-communicating about every bump. This causes chaos. Let the pilot do their job.

Again, they’re getting better on this language.

But another huge policy risk is whether the election outcome places even more emphasis on every Fed nuance.

Mohamed El-Erian on markets, economy, election, Part 2

Non-U.S. monetary policy briefing.

We’ve gone from common shock of pandemic and then inflation surge then inflation coming down.

All global monetary policies followed similar path here so far.

But so far, U.S. is only one who has started easing without huge recession risk.

This is because we are also investing in AI, new energy, etc.

Market expects U.S. rates are higher than rest of the world because of this.

They have to cut more as their economies soften.

We can cut slower because our growth so far is doing well.

Europe can’t invest like U.S. because they don’t have centralized budget. But also because there more risk averse to new investment.

Japan is totally different. They’re finally actually having inflation issues.

China is in a 3-5 year slowdown domestically, which also impacts global growth as a detractor and a risk.

Property trouble in China is a huge factor here.

Property sector overbuilt and over borrowed and now it’s holding back consumption and government bailouts overall.

Mohamed El-Erian on markets, economy, election, Part 3

Our U.S. deficit is 6.4% of GDP even with our strong economy.

You’re supposed to fix the roof when the sun is shining, and we’re putting more holes in the roof.

27 months with unemployment under 4% and deficit at 6.4% of GDP is unthinkable.

We still have runway to fix this.

Quantitative easing is gone. Suddenly we’re much more sensitive to Treasury issuance and pricing.

If Social Security does in fact run out that’s an example of increasing debt and also QE to prop it up.

U.S. is only one to deal with debt by growing faster than debt. This is the good way.

The 3 bad ways to handle debt are austerity or bailouts or default.

So all the odds are stacked on U.S. growth potential. But bailouts are also a common way for U.S. to handle debt.

We’ve been fiscally irresponsible and adding tariff warfare.

Is globalization better?

We assumed trickle down (supply side) works for everyone but it doesn’t work as well for those who need it most.

—

ELECTION OUTCOMES & ECONOMY IMPACT

It’s hard to figure out reaction.

It’s not just who will win.

It’s how will they actually govern.

Will both candidates lead to stagflation?

Trump has said he loves tariffs. If you overuse tariffs, it can lead to stagflation.

Harris loves industrial policy. The right industrial policy doesn’t try to substitute for private sector, and if you do overuse it, it also can lead to stagflation.

—

3 issues El-Erian has explored about how economies get into trouble:

The inability to grow.

The inability of policymakers to bring in fresh thinking.

The lack of proper multilateral cooperation.

When looking at any political leaders you need to look at how these would manifest on their watch.

—

Is AI helping U.S. productivity increase?

If we look at next 5 years, our destination could be great if we manage this bumpy journey.

Better destination is enhancing productivity and AI will lead the way.

If we manage the journey well, AI is labor augmenting. Labor will evolve but AI being labor augmenting is key. (Julian note to self: Need to study this more).

There will be periods of excesses. That’s human nature.

When you talk to leaders (OpenAI, Deep Mind, etc.) they don’t even know where it is headed because it’s moving so fast.

But dollars are there.

Are the energy resources there? Hard to know because we in fact don’t know how fast it’ll move.

—

TAYLOR SWIFT ECONOMIC IMPACT

He told the story of this pic.

Swift economic impact is 0.5% of GDP in cities she goes to. (I think — he went fast on this and I don’t know if it was all cities or KC)

State of Mortgage Tech 2025 & 16 Demo Demo Showcase – MBA Annual 2024

One of The Basis Point team’s most fun business activities is working with MBA on mortgage tech analysis.

We’re honored to host their demo showcases.

We work with the MBA Industry Technology team to analyze, curate, and then showcase the latest in mortgage tech at their conferences.

This year at MBA Annual, we are doing 2 days. I took the shot above while hosting, and it shows the packed house for yesterday. Presenting in this pic (left) is Mike Yu, founder of Vesta, a company reinventing the LOS — a core system of record on the originations side of the business.

I kick off these tech sessions with a State of Mortgage Tech 2025 analysis, and I’ll come back later and blog more on that.

Also see this more detailed State of Mortgage Tech 2025 post.

For now, we want to highlight the 16 companies who are demoing over these 2 days.

They’re from a pool of 130 exhibitors, and representative of every category in the mortgage originations and servicing tech ecosystem.

Check them all out below.

Vesta

Vesta (https://www.vesta.com/)

Product: Vesta LOS

Demo Presenter:

-Mike Yu, CEO

Vesta’s new and modern loan origination system reduces lenders’ operational cost by “inverting control,” guiding users through the loan. This data-driven, task-based approach eliminates manual tasks, enabling your team to focus on what truly matters. With real-time analytics, automated workflows, and unparalleled efficiency, Vesta helps lenders achieve faster closing times, higher loan quality, and lower operational costs.

Candor Technology

Candor Technology (https://candortechnology.com/)

Product: Candor PreQual

Demo Presenters:

-Ed Kourany, Chief Business Officer

-Sara Nakae, SVP Sales and Marketing

Empower LOs with automated pre-Approvals seamlessly from a lenders’ point of sale into their LOS. Candor PreQual, the first and only patented AI-driven borrower pre-qualification service, provides sales and processors near instantaneous borrower insight and decisioning.

SimplyIOA

SimplyIOA (https://www.simplyioa.com/homeowner-insurance)

Product: InsurTech

Demo Presenters:

-Jason Butts, President

-Michelle Sipe, SVP Operations

We specialize in generating new revenue opportunities for mortgage servicers. By applying our data models, aligning with our extensive insurance network, and enabling our industry-leading technology solution, we create a totally unique insurance proposition that puts the customer experience at its core and generates new revenue streams for our partners.

IDIQ

IDIQ (https://www.idiq.com/)

Product: CreditBuilderIQ

Demo Presenters:

-Surya Pochareddy, EVP Strategy and General Manager

-Rick Eggleton, SVP Sales

CreditBuilderIQ: Elevate Your Lending. Close more loans for you and your clients via our powerful credit building platform. We empower mortgage professionals to unlock untapped potential in every applicant, fostering deeper relationships and successful outcomes.

Mortgage365

Mortgage365 (https://mortgage365.com/)

Product: Mortgage365 Platform

Demo Presenters:

-Jason Smith, Director of Business Development

-Joey Revier, Client Success Manager

Mortgage365 is a comprehensive mortgage technology platform designed to streamline the loan process for Loan Officers. It offers a single workspace to manage leads, tools, and loans from start to close, enhancing efficiency and productivity for mortgage professionals.

LenderLogix

LenderLogix (https://lenderlogix.com/)

Product: QuickQual

Demo Presenters:

-Patrick O’Brien, CEO

-Olga Faynshteyn, Business Development Manager

QuickQual by LenderLogix enables loan officers to send borrowers and Realtors a hyper-focused, borrower specific, payment calculator that offers closing cost scenarios, side-by-side comparison of loan products and the ability to update pre-approval letters as prospects shop for their dream home. Loan officers using QuickQual increase their pre-approval to application conversion rate by 40% and get back 30% of their time.

Xactus

Xactus (https://xactus.com/)

Product: Xactus360

Demo Presenters:

-Katy Di Meo, VP Product Management

-Mike Allen, Executive Vice President – West Sales

Xactus360, our proprietary workflow platform, delivers credit reporting, verifications, and settlement services with industry-leading flexibility. Its extensive configuration options streamline workflows, cut costs, and enhance processing speed, security, compliance, and automation—driving business growth.

Calyx Path

Calyx Path (https://www.pathsoftware.com/)

Product: Calyx Path LOS

Demo Presenter:

-Val Barnes, National Sales Consultant

Calyx Path LOS is a cloud-based mortgage technology solution that streamlines lending processes and addresses all your POS, LOS, and mortgage business needs. Backed by over 30 years of industry experience, Path utilizes data-driven strategies and customizable workflows to enhance efficiency and support scalable growth for mortgage lenders of all sizes.

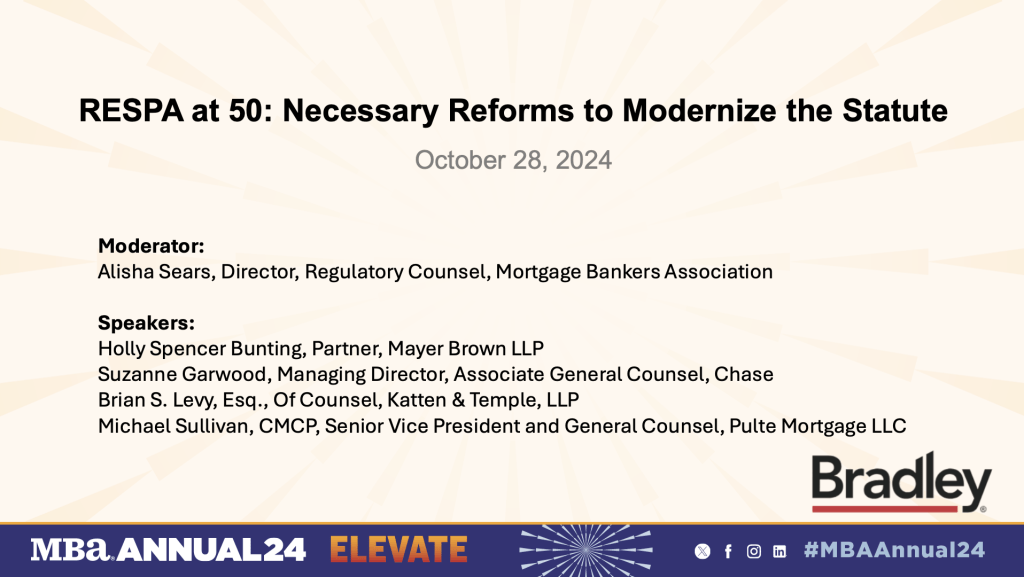

How To Reform 50 Year Old Real Estate Referral Regulations (RESPA)

I missed the RESPA reform panel, but want to touch on it here.

The Real Estate Settlement Procedures Act (RESPA) became effective June 20, 1975.

Regulators were concerned all providers of services in the mortgage process were paying each other referral fees and jacking up consumer fees to cover the referral fees.

Transparency across the ecosystem has evolved quite a bit since then, and RESPA now needs reform.

Think about this from the consumer perspective.

I sign an agreement (required effective August 2024) with a realtor to help find me a home to buy.

I ask them for a good lender go get pre-approved with, and they give me two.

One of those is the lender who is “in-house” with their company.

That lender quotes me lower rates and fees than the other lender I talk to.

Great. I choose them and go forward.

Behind the scenes, there are RESPA rules governing how that in-house relationship could result in financial benefit to the real estate company and/or lender.

But from a consumer perspective they won me based on my comparison of competing quotes.

So am I paying higher costs? No.

These in-house relationships take on many forms (marketing service agreements/MSAs, joint ventures, desk rentals, etc.), and this is a big part of RESPA.

But it’s only one angle. Every other service in the home buying and selling cycle is subject to RESPA rules.

And every service provider (mortgage, real estate, title, etc.) is trying to deliver on the one-stop shop customer experience consumers demand, while also trying to balance RESPA rules.

RESPA has nuanced rules on how every sales and marketing aspect of these services must work.

I ran a mortgage/real estate joint venture from 2008 to 2013 between prominent mortgage and real estate companies, and it was unanimously successful and compliant.

But the MBA is correct to prioritize and modernize these rules that govern marketing and sales of real estate services as vendors collaborate to simplify the process for consumers.

Below are some resources on this topic.

– Read about how MBA seeks to modernize RESPA

Friendlier Consumer Appraisal & Lender Buyback Policies From Fannie & Freddie Regulator FHFA

Fannie Mae and Freddie Mac regulator FHFA announced two key policies intended to help borrowers and lenders.

There’s a policy that says certain loans don’t need a full human appraisal.

Why? Because Fannie and Freddie have so much data on appraisals, a new appraisal isn’t necessarily needed for every deal, and if it’s not, it lowers costs for consumers while still keeping the system safe.

So yesterday (in a panel I had to miss but summarizing here), they announced that these appraisal waivers would be available for even higher loan-to-value ratios (LTV).

This helps save appraisal fee money for people with lower down payments by instead allowing the file to be underwritten with an automated appraisal.

The max LTV ratio eligible for full appraisal waivers will grow from 80% to 90%.

For inspection-based waivers (which means there’s a drive by appraisal instead of a full appraisal), LTV ratio increases from 80% to 97%.

Separately, FHFA announced something else that’ll help lenders.

Normally, when Fannie or Freddie buys a loan from a lender then finds something they deem a defect, they require the lender to buy that loan back.

It’s a source of lots of strain between lenders and Fannie/Freddie.

FHFA said yesterday, that to ease this, they’ll instead apply fees to lenders on certain defect files before mandating a buyback.

This removes burden from lenders, and also enables them to work through defect disputes without overtly having to buy loans back.

It was a program that was in pilot with select lenders, and now it’s more broadly available.

Below are some links from FHFA, HousingWire, and National Mortgage News with more…

– FHFA release on new appraisal & buyback rules

– National Mortgage News on new FHFA appraisal & buyback rules

The Promise & Possibility of AI

MBA chair Laura Escobar moderates Olivia Peterson from Amazon AWS and David Tepoorten from Nvidia.

Nvidia Earth 2 is simulating all global weather to help scientists project weather better.

Digital twins model the real world for this type of analysis.

With Earth 2, this is a monumental leap in weather prediction.

They’re getting this down to 10s of meters to do micro climate projections including wind speeds around buildings in cities.

How can a lender or insurer use this?

They can use it to price insurance models.

As for Amazon, they launched an initiative with the Treasury Department to look at financial impact of climate change.

By 2025, Amazon will have a net zero carbon footprint.

This is even with powering AI with all their data centers.

They’re looking at nuclear power to power AI.

They believe this also has lots of consumer applications.

As for mortgage doc processing Amazon did a quick demo.

Classification is step 1. Determining what kind of doc it is, bank statement, etc.

Then you can use natural language questions to inquire about what’s in the document.

But this demo didn’t talk about where this resides in the mortgage underwriting process.

But extracting data from docs is actually pretty difficult.

The demos that The Basis Point is hosting later today have 3 use cases where we go into contextual detail about how this works in origination and servicing.

We’ll post those below when we’re done.

Amazon also talked about data challenges. You must have clean data and truly single source.

David talked about financial services use cases.

The main use case is digital agents helping employees in customer service centers.

AI assisting the humans who are serving customers is the first key use case both Nvidia and Amazon are excited about for financial services.

MBA Annual State of Mortgage Tech & Demo Showcase – Day 2 (AI Focus)

Day 2 of State of Mortgage Tech and Demo Showcase was focused on AI, and we had another packed house with standing room only.

The state of Mortgage AI is strong not because of Generative AI alone.

It’s because our industry’s fintechs are figuring out how to combine Generative AI with Decisioning AI, including automated loan approval AI the mortgage industry has been mastering since the 1990s.

Below are the Day 2 demos so you can learn more about them.

LoanPASS

LoanPASS (https://www.loanpass.io/)

Product: Decisioning & PPE

Demo Presenter:

-Derek Long, COO

LoanPASS.AI is the merging of the best decisioning and pricing engine on the market with an AI chatbot. Instead of just answering questions, like a typical chatbot, LoanPASS.AI asks the questions needed to get eligibility and pricing for any type of lending product. This combination of a rules based decisioning engine combined with AI delivers an unparalleled level of service for brokers and consumers.

Friday Harbor

Friday Harbor (https://fridayharbor.ai/)

Product: Friday Harbor

Demo Presenter:

-Theo Ellis, CEO

Friday Harbor is an AI-powered originator assistant. It reads borrower documents, identifies red flags and missing documents, and provides 24/7 real-time underwriting. Backed by the Allen Institute for AI in Seattle.

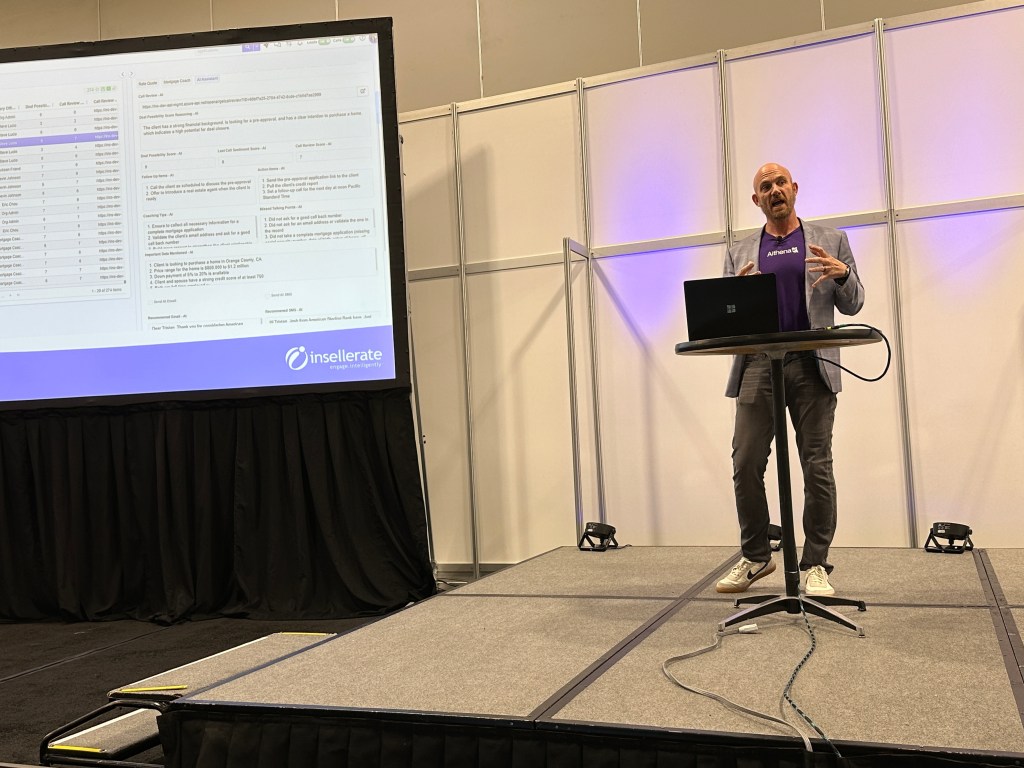

Insellerate

Insellerate (https://insellerate.com/)

Product: Aithena AI

Demo Presenter:

-Josh Friend, Founder and CEO

See how AI is changing the mortgage industry with data from over 200,000 borrower requests. Discover how AI can help your loan officers save time and close more loans.

Sagent

Sagent (https://sagent.com/products/dara/)

Product: Dara AI Docs

Demo Presenters:

-Bart Bailey, VP of Product Management

-Hunter Stair, Sr. Director of Product Management

Dara AI Docs’ core capability is simple: It indexes, classifies, and extracts data from mortgage loan documents. It’s pre-trained with 300+ mortgage documents and extracts 1000+ data points, so it can convert unstructured collateral into searchable, navigable records, and it does this at a rate of 2,200 pages per minute. Then, using the data from those documents — including stamps and signatures — it applies mortgage-specific AI to boost efficiency, accuracy, and compliance in use cases across the loan lifecycle: Advance reconciliation for claims; loan bidding due diligence; income calculation for wage earners; loan boarding; and data audits/reconciliation.

Jaro

Jaro (https://www.tryjaro.com/)

Product: Appraisal QC & AI

Demo Presenter:

-Gareth Borcherds, Managing Director

Jaro uses AI to automate and enhance the appraisal process, delivering faster and higher-quality results. We’ll show how AI improves accuracy and efficiency across every step, from data collection to quality control.

Blend

Blend (https://blend.com/)

Product: Rapid Refi

Demo Presenters:

-Lili Sander, Product Manager

-Marc White, Manager of Solutions Engineering

Reimagine the mortgage experience with unparalleled personalization, automation, and a connected, data-driven origination workflow. This innovative approach supports lenders’ retention and recapture opportunities, driving higher conversions while minimizing loan unit cost economics.

OptimalBlue

OptimalBlue (https://www2.optimalblue.com/)

Product: Compass Edge

Demo Presenter:

-Mike Vough, VP of Hedging and Trading Products

Optimal Blue takes an intentional approach to developing and delivering AI in alignment with a larger mission to help lenders maximize profitability on every loan transaction. These AI assistants in the CompassEdge hedging and loan trading platform are designed to distill complex topics into succinct blurbs that help drive informed decisions, faster. The Position Management Assistant writes a succinct summary of the drivers that cause a change in the risk position of a mortgage pipeline being hedged and the Monthly Profitability Assistant provides a written summary of the top driver that caused a gain or loss of profitability in a pipeline over the course of a full month.

Ocrolus

Ocrolus (https://www.ocrolus.com/)

Product: Inspect

Demo Presenters:

-Vikas Dua, Chief Operating Officer

-Rebecca Seward, Director of Product

Inspect, part of Ocrolus’ Analyze capabilities, leverages Ocrolus’ extensive data capture functionality to help lenders identify and resolve discrepancies between borrower-provided document data and the Encompass 1003 application form. Ocrolus utilizes a direct, productized integration surfaced within Encompass® by ICE Mortgage Technology® to flag data inconsistencies, identify undisclosed information, highlight unsupported application data and easily track resolved findings.

Is Mortgage Bear Market Finally Over In 2025? (MBA Annual 2024 recap)

MBA Annual 2024 was a huge charge for the mortgage industry for 3 reasons.

First, the market is turning.

Total new mortgage units funded will increase from 5.09 million units in 2024 to 6.52 million units in 2025.

This is a 28% increase in units overall.

It’s a 10% increase in purchase loan units.

It’s a 64% increase in refi units.

And it’s not tempered outlook by MBA, because it’s based on rates being 6% most of 2025.

Second, regulators understand how serious the mortgage industry is about balancing systemic and consumer safety with helping more people afford homes.

Addressing affordability irresponsibly can lead to looser loan approval guidelines which can weaken the system overall.

But building more homes and working on Federal — and especially state and local — policy to enable this will help.

This is what new MBA chair talked about as one of MBA’s top 3 housing priorities.

Also MBA CEO Bob Broeksmit talked about how MBA works with ALL regulators and policymakers to advance its goals through full political cycles.

That’s how we ensure housing-friendly policies after the election.

Third, getting everyone together — lenders, servicers, fintechs, and all other housing providers — brings an energy that makes it crystal clear the American Dream of homeownership is alive and burning bright.

This is what we’ve all spent decades committed to.

And when you get thousands of housing leaders together with regulators and policymakers it shows how aligned we really are.

So it’s an optimistic note to head into 2025.

Thanks again to the whole MBA team, and all my industry colleagues for your commitment to American housing.

Happy Halloween, and please reach out or comment below with any questions on topics in this MBA Annual 2024 live blog.