MBA Secondary 2024 LIVE BLOG – State of Mortgage Markets, Rates, Regs, Lenders

Hey folks, here’s The Basis Point Live Blog for MBA Secondary 2024.

This is the preeminent mortgage markets conference each year.

Stay tuned May 20-21 as we update all things mortgage trading, rates, regs, and state of lenders after 2+ challenging years in housing and mortgage.

Below you’ll get all the latest from regulators, lenders, servicers, plus both Wall Street and Main Street perspectives on the housing economy.

We go very fast on this stuff to because it’s truly live, so if your organization is discussed below and you see something is off, please reach out.

And of course please reach out with questions. Some of this stuff is wonkier than our normal analysis and commentary.

MBA Secondary 2024 Table Of Contents

- Good morning from Times Square NYC, site of MBA Secondary 2024

- 2 Handy Mortgage Regulatory Ecosystem Diagrams

- CBS Margaret Brennan on political outlook

- More from Margaret Brennan on MBA Secondary 2024 stage

- Margaret Brennan on U.S. Consumer

- Acting HUD Secretary Adrianne Todman on digital mortgages and helping more homebuyers

- Acting HUD Secretary Adrienne Todman Full Bio

- 2 Month On The Job Update From HUD Secretary Adrianne Todman

- Fed Vice Chair Philip Jefferson On Rates, Economy, Policy – Part 1

- Fed Vice Chair Philip Jefferson On Rates, Economy, Policy – Part 2

- Fed Vice Chair Philip Jefferson On Rates, Economy, Policy – Part 3

- HUB Stage Promo With MBA Chief Economist Mike Fratantoni and The Basis Point Julian Hebron

- Mortgage Market Data Rundown – Part 1 (Bank of America predictions)

- Mortgage Market Data Rundown – Part 2 (MBA Chief Economist Predictions)

- CFPB Director Rohit Chopra on Credit Bureau Fees Hurting Consumers via Lenders

- CFPB Director Chopra On Open Finance

- CFPB Director Chopra: Mortgage Is The Adult In The Room of Financial Services

- A Tense Coincidence On CFPB Targeting FICO

- Tech Showcase On The State Of PPE & Secondary Software

- ICE MT

- Lender Price

- Optimal Blue

- Polly

- Good evening from Times Square NYC, site of MBA Secondary 2024

- GSE Reform: Fate of Fannie Mae & Freddie Mac – Part 1

- GSE Reform: Fate of Fannie Mae & Freddie Mac – Part 2

- GSE Reform: Fate of Fannie Mae & Freddie Mac – Part 3

- Fannie Mae & Freddie Mac Hottest Topics – Part 1

- Fannie Mae & Freddie Mac Hottest Topics – Part 2

- Fannie Mae & Freddie Mac on AI and Tech

- Obligatory Selfies Between Meetings In Midtown

- Sorting Out Bank Capital Rules – Part 1

- Sorting Out Bank Capital Rules – Part 2

- Sorting Out Bank Capital Rules – Part 3

- Sorting Out Bank Capital Rules – Part 4

- Mortgage Servicing Strategies – Part 1

- Mortgage Servicing Strategies – Part 2

- Mortgage Servicing Strategy – Part 3

- Mortgage Servicing Strategies – Part 4

- MBA strategy & team is so tight, they even dress the same!

- Good Night Times Square. Good Night MBA Secondary 2024.

Good morning from Times Square NYC, site of MBA Secondary 2024

Check out how the observation bleachers in Times Square are empty in the morning.

The quiet before the storm.

A good image for a nice quiet post before The Basis Point Live Blog storm…

2 Handy Mortgage Regulatory Ecosystem Diagrams

MBA CEO Bob Broeksmit kicks off MBA Secondary 2024 by taking a mortgage regulatory maze and turning it into 2 handy Venn diagrams.

Zoom in on the images below and study up…

And here are Bob’s full remarks outlining top regulatory priorities for the mortgage industry.

+++

+++

+++

CBS Margaret Brennan on political outlook

MBA Chairman Mark Jones does the first keynote fireside chat with CBS’ Margaret Brennan on election, geopolitics, and how they may impact markets.

Reminder: before Brennan was one of the top political media figures in America, she came up as an on-air financial journalist at both Bloomberg and CNBC.

+++

Trump beating Biden in Arizona by 5 points in Arizona, a state Biden won.

Independent candidate RFK will take votes from both primary party candidates in a close race.

Foreign policy is on the ballot for all Americans regardless of whether they typically vote this way or not.

Here’s why:

4 multi-front wars involving allies in Middle East alone (not including Ukraine).

Active tension with China.

China and a Russia aligned on building trade relationships.

85-year old Iran supreme leader, not president who just died in helicopter crash, is who rally runs the country.

The leader who just died was a successor.

Leader of one of largest U.S. allies (Israel) is completely ignoring U.S. president.

Next president has their hands all the way full on foreign policy.

We’re not fully calculating how much Gaza conflict will impact elections and future terrorism risk.

Terror attack risk in America is a huge risk.

Trade war with China and tariff policies are a hot topic and will have immediate impact.

More from Margaret Brennan on MBA Secondary 2024 stage

Dehumanization of death in Israel v Hamas war is way different in America v Israel.

This issue is grey and way more complex than a bumper sticker and a tweet.

But the American public is too polarized and it becomes black and white.

If China took over Taiwan…

Policymakers in China look to a slow strangulation of Taiwan more than an invasion.

Strangulation the erosion of democracy slowly.

Cyberattacks.

Closing off media.

Sound familiar?

China is taking notes on what Russia is doing in Ukraine too.

Ukraine now requesting more weapons from U.S. to defend new fronts that Putin says they’re not after — but they are.

This fight won’t go away.

There’s no immediate end.

All diplomatic talks are just game strategy. The conflict will continue.

Margaret Brennan on U.S. Consumer

Inflation issue has most direct influence on politics now.

People see numbers literally move in front of them when they pump gas or look at grocery store checkout.

TBP Note: meanwhile the wonks exclude gas and food from Core inflation readings.

Supply chain is stabilizing but prices in the real economy are still too high.

We hear from left and right “why are you spending money abroad when we’re struggling at home,” and the candidate that can answer this clearly will benefit.

They must constantly explain the choices they’re making.

But this is hard in the cacophony of social era.

Next tax package…

Yellen said nobody below $400k per year won’t see any tax changes.

Acting HUD Secretary Adrianne Todman on digital mortgages and helping more homebuyers

Reduced access to mortgage credit in last 3 years by allowing rent to count as good credit.

For those who don’t follow this closely, on-time rent payments are not on credit reports so allowing lenders to count rents as good credit makes mortgages more approvaable for more people.

20yr high for homeownership rates.

$38b in e-notes have been securitized.

This is a major development in responsible digitization of mortgage.

Now this will be part of normal securitization pools.

This is a key step toward normalizing digital mortgages.

And digital mortgages make data more available which makes servicers faster to help borrowers during hardships.

Acting HUD Secretary Adrienne Todman Full Bio

Adrianne Todman is Acting Secretary of the U.S. Department of Housing and Urban Development (HUD). She was previously confirmed by the Senate to serve as the Deputy Secretary of HUD in June, 2021. As Deputy Secretary, she served as the second highest ranking official at HUD, and executed both policy and operational priorities. This included providing guidance on department-wide initiatives to increase housing supply, improve disaster response and recovery efforts, steer climate and resiliency endeavors, and enhance customer access to HUD’s programs. Additionally, she oversaw HUD’s efforts to improve agency hiring and workforce engagement, and enhance the agency’s risk assessments, IT investments and contracting protocols. Prior to joining HUD she served as the CEO of the National Association of Housing and Redevelopment Officials (NAHRO) from 2017 to June 2021. During her tenure, she improved the association’s financial standing and business operations, created a member-centric culture, and advocated for funding and policies to preserve and develop affordable housing and help communities thrive. Before joining NAHRO, Acting Secretary Todman served as the Executive Director of the District of Columbia Housing Authority (DCHA). At DCHA, she implemented a national award-winning model to house veterans experiencing homelessness, increased homeownership opportunities by 50 percent for low- and moderate-income families served by DCHA, increased the number of affordable units available in neighborhoods experiencing rapid growth, and oversaw multiple redevelopment efforts. She prioritized repairs to units, services for youth, workforce development, and commissioned the first citywide needs assessment of public housing residents. Acting Secretary Todman previously served in several career positions at HUD. First, as a manager of HUD’s $500 million grant competition that focused on revitalizing distressed public housing sites, and also as a policy aide in the Office of the Secretary where she worked with staff across HUD’s programs. Her career in public service began in the office of then-Congressman Ron de Lugo, a long-serving member representing the U.S. Virgin Islands, where Todman was born and raised. Acting Secretary Todman believes that we have a responsibility to confront housing insecurity; increase and preserve the nation’s housing supply; eliminate housing discrimination; and support community resiliency, particularly following a natural disaster. She has focused on ensuring that HUD has the staff and tools it needs to administer and provide oversight over programs critical to supporting people and communities across the country. She is a graduate of Smith College and lives in Washington, D.C.

2 Month On The Job Update From HUD Secretary Adrianne Todman

MBA Chairman Mark Jones sits down with acting HUD Secretary Adrianne Todman.

Todman grew up in Virgin Islands and is now in a White House cabinet position.

Using “the power of the perch” to show people how Federal government can help them.

We want to tell people about down payment assistance, housing counseling, and rental program help.

MBA chairman and president Mark Jones lauded the HUD support of FHA 203k loans, which enable home rehabs.

This is a key product for lower to middle income people.

Todman addressed need for (and how this product helps) modernized homes to be resilient to climate and keep utilities costs down.

Accessibility…

She use to develop homes and said “I’m a supply person” and understands people need help on affordability.

Talking to other developed market counterparts. For example in Germany, they’re half rental and half mortgage. U.S. ownership rate is higher.

Fed Vice Chair Philip Jefferson On Rates, Economy, Policy – Part 1

Jefferson is vice chair of the Federal Reserve board of governors.

Economic outlook…

GDP up 1.6% for 1Q24 vs 3.4% from 4Q24.

3.1% spending growth for 1Q24 was similar to second half of 2023.

Improving supply has helped to bring inflation down.

Labor market solid: 175k jobs last month, and 240k jobs YTD. Workers 25-54 participating more in job market than pre-pandemic.

Inflation eased dramatically. Core PCE hotter in early 2024 than late 2023, but still down from peaks.

Too early to tell but the better CPI April reading is encouraging.

Long term inflation expectations for next 10 years is close to pre-pandemic levels.

+++

Fed Vice Chair Philip Jefferson On Rates, Economy, Policy – Part 2

FOMC won’t reduce target rates until inflation looks sustainably close to 2%.

We’re reducing balance sheet.

$60b to $25b per month for treasuries.

$35b for agency MBS and reinvesting proceeds into treasuries.

Housing is most interest rate sensitive par of economy.

Mortgages were about 3% before Fed hikes.

Rates surged as Fed hikes and mortgages fell significantly.

This brings supply and demand into balance and reduces inflation.

Housing costs make up a large share of household budgets.

A home costs is using rents instead of ownership costs because ownership is partly an investment.

Thea costs take a long time to come in. See chart.

Despite higher rates, people took our $1.5 trillion in new loans in 2023.

+++

Fed Vice Chair Philip Jefferson On Rates, Economy, Policy – Part 3

MBA Chairman Mark Jones and Chief Economist Mike Fratantoni sit down with Fed Vice Chair Jefferson.

Mike asked about quantitative tightening, aka reducing balance sheet holdings of Treasuries and mortgage backed securities.

Jefferson said they’re doing this very carefully. See post above with figures of monthly reductions.

He also noted that nobody knows what the appropriate balance sheet size is. Main goal is not causing undue disturbances in capital markets.

If there’s too much selling of these securities, it pushes security prices down, and rates up.

So far housing market and economy has handled higher mortgage rates.

But may not be able to handle much more.

Jefferson highlighted the critical need for dual mandate: price stability and full employment.

Cautiously optimistic we’re returning to balance with dual mandate.

Then rates would come down.

+++

HUB Stage Promo With MBA Chief Economist Mike Fratantoni and The Basis Point Julian Hebron

Pretty cool to see the promo here! Mike is a legend. Honored to be on this board with him!

Mortgage Market Data Rundown – Part 1 (Bank of America predictions)

Bank of America mortgage backed securities strategist Jeana Curro shared the stage with MBA chief Mike Fratantoni to run down lots of data.

Below is a quick recap, and later I’ll follow up with some charts.

BANK OF AMERICA – JEANA CURRO

Outlook:

10yr Note 4.25% by year end vs. 4.44% now.

6.5% 30yr fix mortgage rates by year end vs. 7% now.

2.25% spread between 30yr fixed and 10yr Note vs. 2.56% now.

Rates, volatility, macro policy create our outlook.

We predict mortgage bonds will outperform.

This would be good: rates drop if mortgage bonds rally.

We think first cut in December, then 4 cuts 2025, 2 cuts 2026.

Fed bond selling (QT) to end year-end 2024.

Terminal rate 3.75% vs. 5.25% today.

Mortgage Volume Outlook:

$1.6t, with $1.36t purchase (85%), and $240b refi (15%).

New home sales big contributor to our forecast.

We think they increase 11% this year.

This is historically consistent.

No lock-in effect with new home sales. Builders (unlike private homeowners who don’t want to ditch their low rate) are highly motivated to sell.

They can offer lower rates via buy downs.

Key takeaways for lenders:

On volumes, lenders have adjusted accordingly. Large lenders look for death, divorce, downsizing.

Prepay speeds slow with rates >5-6%.

Affordability is tough to find affordable properties that meet GSE LIP/VLIP requirements.

On second mortgage opportunity, there’s $18t in tappable equity (leaving 20% equity in system).

Even with all this, there’s only been $21b in second lien issuance.

This is super low. The GSE second mortgage program, led by Freddie Mac so far (but Fannie Mae will likely follow) can add $1.8t to this.

Government programs will provide standardization in second mortgage market.

Most of BofA Jeana talk with investors has been about Freddie Mac second mortgage proposal.

“If I have all this equity I can get a second mortgage or sell my home. But I’m locked in so I probably stay.”

Does owning second lien or HELOC make me more or less likely to refi my first mortgage?

Demand side for MBS…

Money managers own 5-7% more than index (overweight).

More will come in when spreads are attractive.

Fed continues mortgage backed securities runoff though monthly pay downs.

But these paydowns are lower than $35b cap.

Fed has telegraphed a lot they want to be mostly Treasuries.

Among investments BofA mortgage team likes is Texas properties and non-owner-occupied stuff.

Mortgage Market Data Rundown – Part 2 (MBA Chief Economist Predictions)

MBA CHIEF ECONOMIST MIKE FRATANTONI PREDICTIONS

Mortgage market outlook:

We predict 2 Fed cuts this year.

Mortgage volume of $1.81t this year.

Delinquencies 3.94% v 3.8% unemployment. Super low and super correlated to unemployment.

This is good news on mortgage market safety.

There are 5m more people in America than previously thought.

This means more demand and less affordability.

Homeowner vacancy rate low as it’s ever been. Rental vacancy rates up because multi-family construction coming to market.

Typically it’s about 10% of inventory is new constitution, and now it’s a third.

Realtor listing count is up in April.

Applications for loans to buy homes down 15%.

KEY: But applications for loans to buy newly built homes up 22%.

Average new home loan size is coming down. Size of new homes smaller. Builders get it.

New housing starts, new home sales, existing home sales all projected to be up 2024, 2025, 2026.

First time homebuyer activity…

Lots of demographic demand: 50m people between 30-40 right now.

First time buyers are struggling with affordability.

Consumer also getting strained outside of housing. Delinquencies rising on non-housing debt.

FHA is a critical source of first time buyer lending, with FHA loans being north of 80% for first time buyers.

This is also true with new homes. (CHART COMING)

FHA debt-to-income ratios are rising.

SPREADS…

30yr mortgage minus 10yr treasury.

Thinning spread isn’t good news for mortgages, it’s bad news for treasuries. Too much treasury supply.

Also see charts for Conventional/FHA spread and Conforming/Jumbo spread.

Jumbo normally 25bps higher. Then jumbo went lower by as much as 60bps before March 2023 bank crisis. Now jumbo is 15bps lower. Still because of banks not securitizing and using non-interest bearing deposits as low cost of funds for funding jumbos.

Now 8 straight quarters of negative profitability.

It’s less bad now because of higher rev, not lower expenses.

MORE CHARTS COMING ON ALL OF THESE TOPICS…

CFPB Director Rohit Chopra on Credit Bureau Fees Hurting Consumers via Lenders

CFPB Director Rohit Chopra focused on credit bureaus and how credit scores are obtained for loan approvals.

Because credit scores are required for loan approvals, lenders have to typically pay twice.

Once when approving loans and once when funding.

And then more fees for co-borrowers and for the securitization process.

So lenders pack these fees into overall lender costs including fees and rates.

Single credit reports are $18-40. Equifax, TransUnion, Experian have a lot of pricing power.

Flat fees went up last year from FICO for trimerge reports.

They also raised prices for soft pulls.

Soft pulls grew so lenders could check credit without triggering marketing alerts that flood borrowers with lender pitches.

They used to be cheaper. They’re not now.

Rapid rescore fees also went way up. But this is the result of bad data in credit reports.

Also employment certifications via things like Equifax The Work Number.

Some borrowers increase loan costs to cover these fees. All of it leads to higher lender fees.

And this is especially tough for borrowers who are already challenged by affordability.

The Fair Credit Reporting Act will be used to fix these issues with fee caps.

This is “price gouging.”

+++

NOTE: Here are CFPB Director Chopra’s prepared remarks. Notes in this post also include remarks made live.

CFPB Director Chopra On Open Finance

[continued from above]

The CFPB and FHFA will work together to assess mortgage pool data to maybe save borrowers money by not needing repeat credit fees.

Credit bureaus are “taking a tax, running a tollbooth” to collect these fees and that’s bad for all of us.

+++

MBA chief Bob Broeksmit asked about CFPB being ruled constitutional.

Director Chopra said they’ll look at more enforcements across consumer finance.

But he did say mortgage had been the adult in the room.

Chopra said (correctly) that unwinding consumer protection laws would be chaos. True.

Loan officer compensation rules were to prevent mischief on steering borrowers to more expensive loans.

We’re going to look at all rules, but we haven’t looked at this again yet. When we do, we’re happy to work with mortgage industry to ensure lawful practices.

We’re more focused on making loan modifications seamless in mortgage servicing.

+++

NOTE 1: Here are CFPB Director Chopra’s prepared remarks. Notes in this post also include remarks made live.

NOTE 2: Here’s an MBA letter to FHFA director Sandra Thompson with recommendations on creating competition in the credit reporting space.

CFPB Director Chopra: Mortgage Is The Adult In The Room of Financial Services

Lenders must use CFPB enforced forms to disclose fees and then we’re told they’re junk fees.

Chopra said junk fees are when there’s no real competition.

We have a mortgage system that’s fiercely competitive mostly.

But there are credit and other verification fees that aren’t competitive.

Borrowers and lenders are told what vendor they can go to, not who they can choose.

Good talk and director Chopra was very open with the mortgage industry today.

He said again that the mortgage industry is the adult in the room in financial services industry.

+++

NOTE: Here are CFPB Director Chopra’s prepared remarks. Notes in this post also include remarks made live.

A Tense Coincidence On CFPB Targeting FICO

Whoa … FICO was the sponsor of the last MBA Secondary 2024 sessions with CFPB Director Chopra.

Read the segments above and you’ll know why that’s a crazy coincidence.

Sharp regulator remarks that name names. Followed by one of those names getting highlighted as a sponsor of the session in which the remarks where made.

The room palpably murmured when FICO went up on the screen.

Brief tensions like this happen when all players in a giant industry with $2 trillion per year in originations and $14 trillion in outstanding servicing come together.

Good conference organizers (and MBA is among the best) try to consider appropriate pairings of content and sponsor mentions without watering down content.

But no conference team can perfectly balance how/when content and sponsor promos pair up.

Especially when a regulator targets certain industry players by name without first letting conference organizers know.

And make no mistake: America’s top consumer finance regulator doesn’t need to pre-vet their content with any conference organizer.

So, it’s a five-second “whoa” moment at MBA Secondary 2024.

But here’s the real takeaway:

This was the most important and productive industry/regulator dialog of 2024 so far.

Twice during his segments, director Chopra said unprompted that mortgage is the adult in the room of the financial services industry (both noted in segments above).

Tech Showcase On The State Of PPE & Secondary Software

This year, MBA invited us to host their first-ever MBA Secondary Tech Showcase specifically dedicated to PPE & Secondary systems (aka, the lifeblood of your business). From first touch with consumers and LOs through secondary operations, these systems are the glue across your full tech stack.

Joined by special guest Giuseppe Grieci (Freddie Mac’s Director of Pricing Strategy), we hosted 4 rapid-fire 8-min demos from Lender Price, Optimal Blue, ICE Mortgage Technology, and Polly. Each was followed by 4 mins of Q&A with me and Giuseppe.

If you missed it live, check out below to see how this software category has evolved, and where it’s headed next. And if you like what you see, contact the companies directly to hear more. Or hit us, and we’ll put you in touch.

ICE MT

ICE Mortgage Technology (icemortgagetechnology.com)

Product: ICE PPE

Demo Presenters:

– Jenee Robinson, Director Product Management

– Tom Lyons, Solutions Specialist

ICE PPE is the only product and pricing engine natively built into the Encompass digital lending platform. It enables users to easily find products and pricing, check guidelines and eligibility, lock and update loan pricing – from within a stable, reliable end-to-end platform. Visit ICE’s website for more information about ICE PPE or contact brad.yahrling@ice.com.

Read the product press release (May 15).

Lender Price

Lender Price (lenderprice.com)

Product: Base Price Solution | Bulk Price API

Demo Presenters:

Paul Orlando, Chief Strategy Officer

David Colwell, EVP Business Development

Base Price Solution (BPS) by Lender Price was specifically designed for capital markets and secondary marketing teams to automate their base price creation. The product significantly reduces the need for spreadsheets, improves accuracy, and enhances profitability. Providing direct integration for TBA pricing, lenders are able to set up pricing plans for different types of products and reference buy-up and buy-down tables and MSR servicing grids imported into the system.

Additionally, BPS allows manual channel-based subsidies at the coupon and interest rate level and complete traceability for audits. With BPS, lenders can quickly reprice within minutes during market swings and recall any committed pricing date to the history screen for reference or audit purposes. By automating the process, lenders save time, ensure competitive pricing, and reduce the risk of manual errors. Visit https://lenderprice.com/bps for more information.

Read the product press release (May 17).

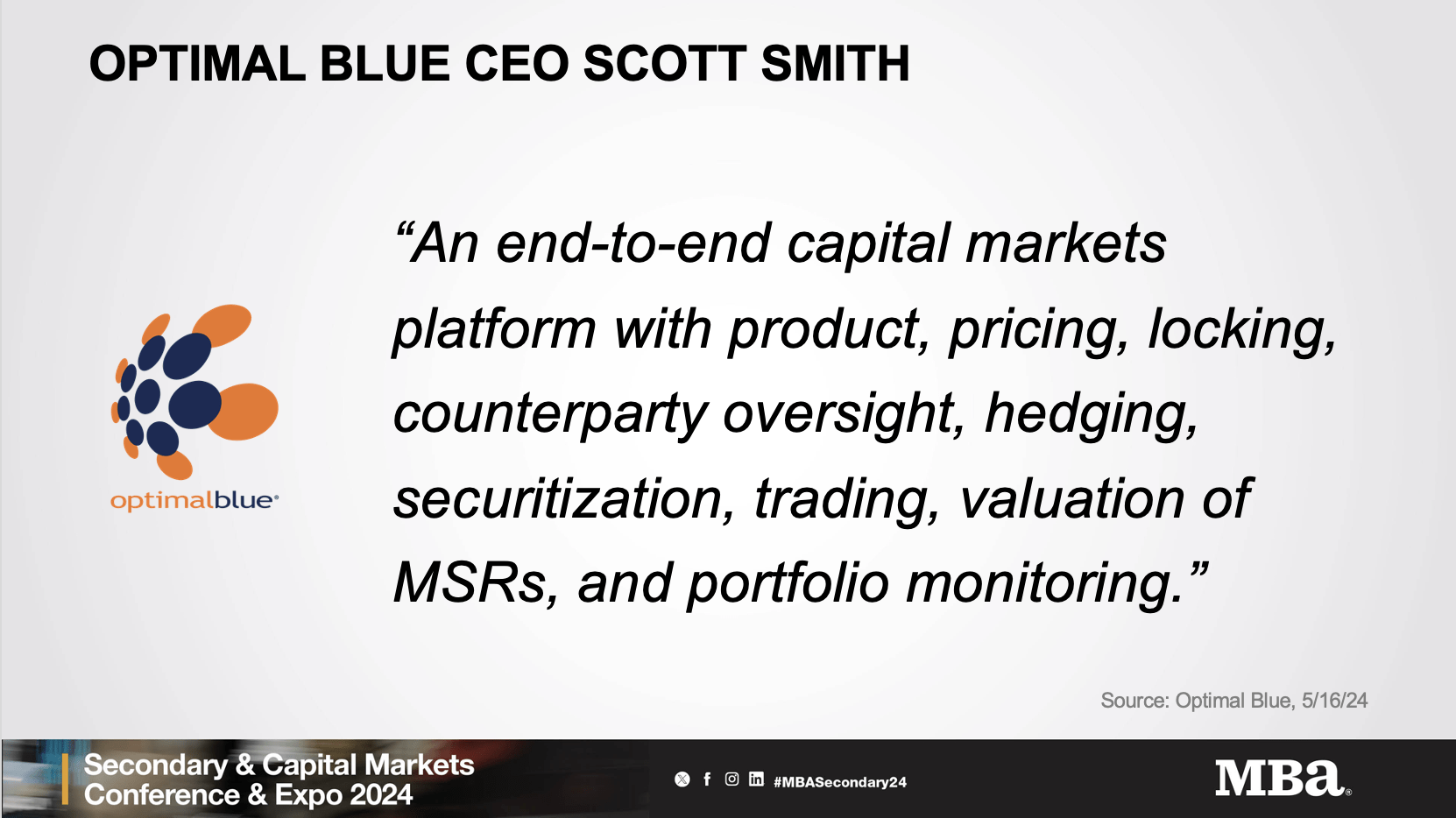

Optimal Blue

Optimal Blue (optimalblue.com)

Product: Optimal Blue PPE | CompassEdge

Demo Presenters:

Mike Vough, Vice President Hedging & Trading Products

Erin Wester, Vice President Product Management

Optimal Blue helps lenders optimize their competitive advantage by taking control of their margins – from pricing accuracy to pipeline risk management, and every step in between.

Optimal Blue connects the primary and secondary markets – helping lenders offer American borrowers the very best product and price on the front-end while simultaneously helping secondary teams fine-tune profitability in their hedging and trading strategies. The demo covered advantages that come with Optimal Blue’s API-first, open-network approach to the market, as well as the competitive value to be gained through Optimal Blue’s market-representative, real-time data.

Request a demo to hear about the latest enhancements to Optimal Blue’s core platforms: the Optimal Blue PPE and the CompassEdge hedging and loan trading platform, including an explanation on how lenders benefit from a continuous feedback loop between front-end pricing and secondary departments via the integration of the platforms.

Optimize Your Advantage with Optimal Blue’s comprehensive capital markets platform.

Read the product press release (May 16).

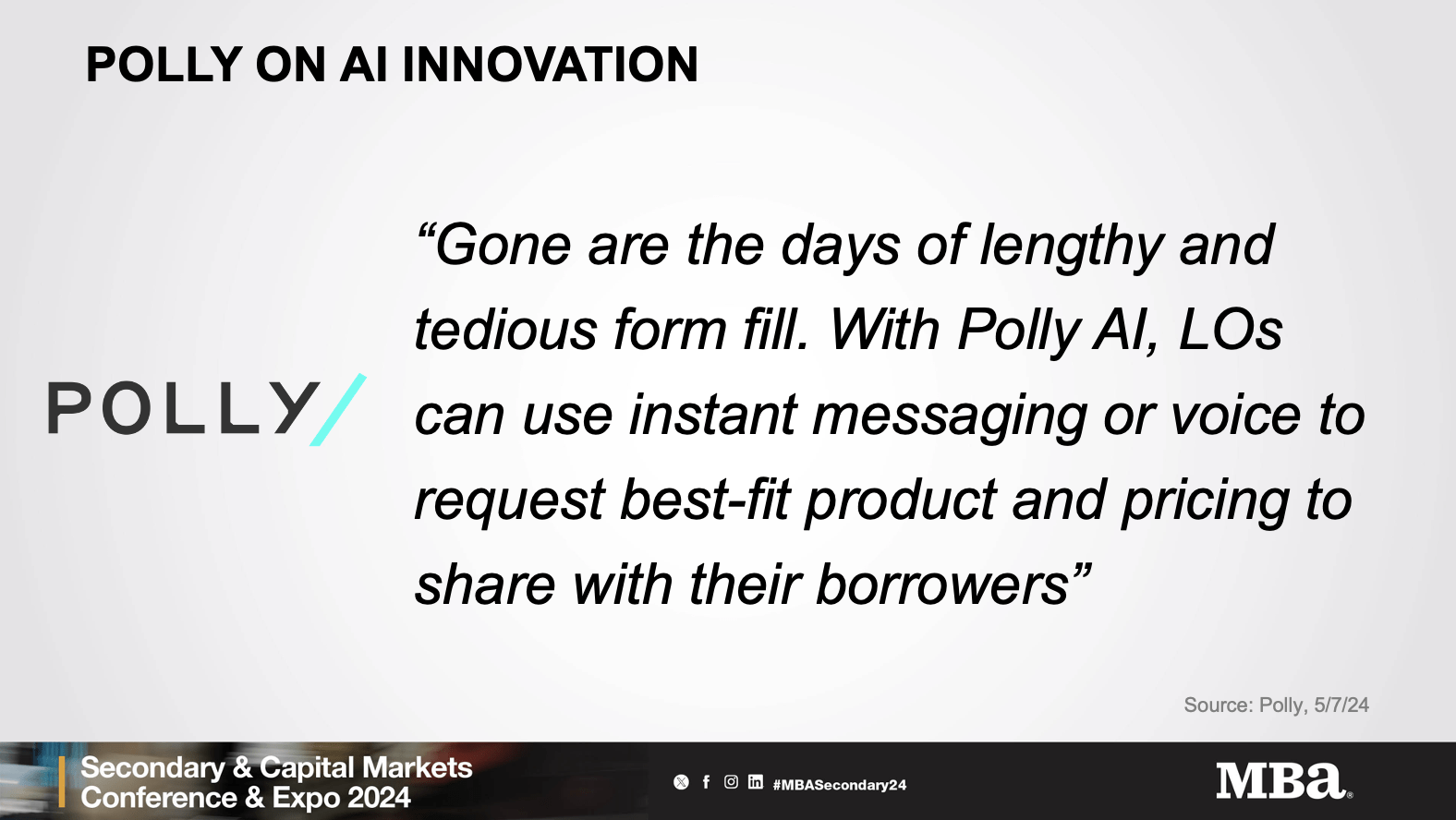

Polly

Polly (polly.io)

Product: Polly AI

Demo Presenters:

Troy Coggiola, Chief Operating Officer

Jon Foy, Vice President Product & Design

Polly operates the mortgage industry’s first and only cloud-native, commercially scalable pricing engine. Since its introduction in 2019, Polly has continued to propel unmatched innovation and functional depth that enables lenders to turn their secondary and capital markets function into a high-performing profit center.

Read the product press release (May 7).

Good evening from Times Square NYC, site of MBA Secondary 2024

Here’s the shot as the evening sun streaks through the buildings onto the Times Square observation bleachers. Pretty cool…

GSE Reform: Fate of Fannie Mae & Freddie Mac – Part 1

We’re close to 16th anniversary of Fannie and Freddie being put into conservatorship.

FSOC report on Nonbank mortgage firms is rough even though nonbanks showed up after the last 2 crises.

Sometimes Washington shows up with flowers and sometimes a knife.

The election will be rough and impact fate of Fannie and Freddie.

These aren’t the same orgs as 2007-2008. They’re so much better.

But like football or diets, the last part is hardest.

In DC, things are impossible until they’re inevitable.

Jonathan McKernan could be the FHFA head, who worked for FHFA under previous head Mark Calabria.

He also would advocate for ending conservatorship.

Isaac Boltansky: I had twins last year and wanted to name them Fannie and Freddie so I could see them unable to get out of their cribs.

Jaret Seiberg: if you can’t bring private label securitization market to legitimately compete with Fannie and Freddie, releasing them is something we should be careful about what we wish for.

GSE Reform: Fate of Fannie Mae & Freddie Mac – Part 2

Jaret: nobody is going to vote for you if you release Fannie and Freddie.

If you get no political upside and lots of potential downside, why would you support that.

Both Biden and Trump would be second term, but that doesn’t matter as much. It’s too risky politically.

Isaac: you’ve seen no engagement from Biden administration on releasing Fannie and Freddie.

You have $4t in Trump tax cuts expiring and need $4.5t to extend for 10yrs, and a $320b capital question for Treasury with Fannie and Freddie.

How do you determine what Fannie and Freddie should earn if released.

A second Biden administration wouldn’t really address these, but Trump might.

Jaret: Social security and Medicare depleted, and these are bigger issues.

Both: Fannie and Freddie are capitalized but Treasury has first rights to all that capital, so really we’re nowhere on releasing them.

Even with Trump, you don’t know who he’d select as Treasury and anyone who says they know is wrong.

You’ll also have year one of non-focus on this so when you get to 2026, you also have debt ceiling.

GSE Reform: Fate of Fannie Mae & Freddie Mac – Part 3

Isaac: You have Treasury warrants that are 80% of Fannie and Freddie equity. These expire in 2028.

This can overshadow any excitement in investment community about releasing them.

$320b in senior preferred, which Treasury has first right of refusal to.

If money doesn’t flow to investors (which it doesn’t really because of these Treasury preferences), how do you raise money.

Jaret: you can assign values to these figures (above) but it’s not worth what all the math says they’re worth.

MBA chair Mark Jones said even if Fannie and Freddie are released, there still needs to be explicit guarantees of mortgage backed securities.

The government can’t allow defaults on these GSE securities. In release, you’d have to make a law for this guarantee.

Again, it’s a political will question.

Isaac: Stories matter more in DC than spreadsheets.

Key: The only thing that’s going to matter is engagement and educating these politicians.

Editor note:

And that’s where the MBA can be quite helpful — as CFPB director Chopra said yesterday, the mortgage industry is the adult in the room in financial services, and that goodwill comes into DC and regulators via the MBA, and this will help a lot once the election happens and this Fannie and Freddie issue comes up again.

Fannie Mae & Freddie Mac Hottest Topics – Part 1

Sonu: 52% of loans we bought were first time buyers.

How did we do it in 3 ways.

1. Down payment assistance. Free matching of lenders to local down payment assistance. Will cover full country by end of 2024. Also special purpose credit. This is programs for mostly families of color.

2. Tech. Making more borrowers with thin credit files better able to qualify. AIM risk relief for lenders is a huge focus too.

3. Educating consumers. Credit Smart in English and Spanish to help folks become homeowners. Also helping people built credit — enrolled half a million people to use rent to built credits scores. And 55k of these people have credit for the first time.

4000 lenders use the down payment assistance program and more can sign up at dpa1.freddiemac.com.

Devang: We won’t sacrifice housing stability for affordability. We won’t expand credit box just to accommodate.

We can control market overall. But we can help address down payment assistance.

This is HomeReady, our 3% down program with lower mortgage insurance.

We also have $2500 credit program.

The HomeReady Assist program is actual down payment assistance.

Appraisal tools have saved $52m.

Helping the credit invisible by making 520k units qualify for rental monitoring.

We’ve helped people increase credit scores 40 points.

If you lenders use D1C for income and asset verifications, you get rep and warrant relief.

We’re also using AI to help multiple language borrower education.

Fannie Mae & Freddie Mac Hottest Topics – Part 2

Sonu on second mortgage program (Freddie Mac’s proposal to help second mortgage market).

6 of 10 borrowers feel locked into first mortgage but have equity and second mortgage program is way to enable them to use their home as an asset.

Devang on loan repurchases…

We’ve reduced repurchases 50-60%.

New approach: Notice of potential defects instead of just requesting repurchases.

We have heard lenders on this.

The 2023 loan quality has improved industry wide.

Our North Star is to get out of repurchases altogether and machine learning can help mature our notice of POTENTIAL defect program.

This means lenders can correct any issues BEFORE sale.

Sonu on repurchases…

We looked at loan level issues to understand how to trim repurchases and increase loan quality.

We’re down 60% from peak in 2022.

We wanted to make sure using 14 lenders as a pilot to get this done within rep and warrant framework.

Fannie Mae & Freddie Mac on AI and Tech

Sonu on AI:

Tech is part of all decision making.

Two goals:

1. How do we help thin credit: with LLPA policies that incentivize lenders to help.

2. Using AIM program to provide rep and warrant relief to lenders for using our AIM framework, which includes tech vendors vetted by Freddie Mac.

KEY: Lenders are seeing 14% lower cost helping these borrowers with our AIM tech framework.

Devang on AI:

Reputation risk is key for us on AI.

Appraisal modernization with AI is the biggest priority.

We have 6b property photos and all property data and this is great for training AI models.

A critical AI training issue is removing bias.

AI has the potential to solve this but AI models in their early days can have human bias that may have already been in datasets.

Sonu to lenders: we need your pushback on how we can improve.

The repurchase issue is a great example of how it works to improve with pushback.

Also KEY for lenders: Use our loan cost tools. They WILL lower cost for you.

Obligatory Selfies Between Meetings In Midtown

Smile!

Or maintain game face.

Not much of a solo selfie dude, but they actually don’t let you leave Times Square without doing it now…

Nasdaq background…

+++

North side background…

Sorting Out Bank Capital Rules – Part 1

Deb Jones: Market consensus is that Basel III may be over-indexing on capital requirements.

Housing is such a huge part of U.S. economy, which can hurt overall economy.

It’ll also maybe shift investment outside U.S. overall.

Matt Bisanz: For capital requirements, commerical is 8 cents on the dollar, and this includes warehouse lines. Mortgages are 4 cents on the dollar for capital requirements.

Basel III proposal adds a lot of granularity to the standards.

This makes higher LTV loans more risky as example.

Also new proposals are based on incentivizing publicly traded, investment grade firms.

This means nonbank lenders (aka IMBs) which make most mortgages, are at risk.

So are banks providing warehouse lines to those nonbank lenders by investment grade banks.

Deb Jones: CRA and high LTV initiatives are also at risk here for banks and lenders.

When you add more capital holding to these programs for lower income borrowers, it makes costs for these borrowers more expensive.

The LTV proposal doesn’t even account for mortgage insurance inherent in higher LTV loans.

If banks want to hold fewer MSRs because they run out of room, does it mean we write down value of mortgages?

Also it may make it harder for IMBs to sell loans.

THE BASIS POINT 2 KEY QUESTIONS:

1. Do more loans go to private market? Could be good but more viable for jumbos, which are already predominantly a private market product.

2. And do the GSEs have all the more pressure on trying to help with affordability?

Sorting Out Bank Capital Rules – Part 2

Matt VanFossen on impact to nonbank mortgage lenders (aka IMBs):

Proposed regs don’t apply to IMBs directly, but they’re hit because the banks who provide warehouse lines for IMBs to fund loans will pull back.

This will lead to a pullback in serving underserved communities that the nonbanks (IMBs) dominate.

This ultimately is a direct impact to lending to communities who need the most help.

Fran Mordi: MBA is pushing hard to educate regulators on warehouse lender risk weighting.

That by itself is an issue in Basel III proposals.

Matt VanFossen: We’re already seeing warehouse lenders exiting the market.

Deb Jones: Investors are already pricing in proposed regs for banks.

If investors don’t see banks building up capital now (even though Basel III isn’t in place yet), their stocks can drop, potentially further straining capital goals.

Matt Bisanz: If we’re trying to get to no risk — aka no bank failures, which is an implicit regulator goal — rather than low risk, you cut off key parts of the consumer.

Regulators aren’t saying to stop warehouse lending.

They just want banks to take a close look at concentration of their warehouse businesses.

Deb Jones: As an industry, we’re doing advocacy after the fact. Reactive.

It’s important that we all work with MBA, HPC, ABA, etc. to learn and help regulators learn how Basel III would permeate and impact bank/lender ability to serve consumers and businesses.

THE BASIS POINT NOTE:

Select banks failed and that’s a regulator issue with that bank, not an industry wide issue.

Basel III well intended, but we need to work together to balance systemic safety goals and properly serving businesses and consumers.

Sorting Out Bank Capital Rules – Part 3

Matt VanFossen: Mortgage delinquencies are record low (3.94%) in U.S.

So these Basel III international bank standards are incongruent with this U.S. mortgage performance.

Matt Bisanz: If Jamie Dimon is meeting 15 times with regulators to refine Basel III for securities trading, then other issues (like Matt V covers above) get less attention.

So we need to focus on making sure that housing finance is understood in this proposed regulatory framework.

THE BASIS POINT NOTE:

IMBs are not a fundamental systemic risk issue.

If one goes away another replaces it without systemic disruption.

Regulators need reminders of this.

And politicians definitely use “nonbank” as a pejorative for political convenience without fully getting the stability IMBs bring to America’s housing economy.

Sorting Out Bank Capital Rules – Part 4

[continued from above]

There are thoughts on splitting Basel III in Washington.

There’s been a lot of focus on securities (see Jamie Dimon reference in previous post above), so one thought is: Implement that part of Basel III first, then maybe implement lending?

Deb Jones questioned which one might macro economy most.

Good question.

A case can be made for either one, but lending arguably hits the real, on-the-ground economy for businesses and consumers most.

Final note from Matt VanFossen: The proposal may change what a defaulted loan is.

If a consumer mortgage is late more than 90 days, industry still trying to figure out how much more capital will be required.

Great panel on a critical topic.

Further Reference:

Mortgage Servicing Strategies – Part 1

![]()

We have an orphaned block of servicing now, and have never seen it with inverted yield curve.

Normally this means less volatility, but that’s not the case now.

The low coupon has almost no prepayment risk.

Why would I ever hedge that.

You hedge cash flows that are the escrow balances.

The value change in a 100 basis point market change would be in the escrow balance cash flows.

Having payment shock on taxes and insurance (escrow balances) is also a first.

The 2-3% coupons are not something you have to worry about much.

But there is risk in 4-5% coupons because rate market can get us back to this range.

Mortgage Servicing Strategies – Part 2

At a bank, you have other revenue with deposits, etc.

At an IMB, you have to manage risk much more carefully.

Escrow accounts in a servicing book are like gold right now.

If you’re using a sub-servicer vs. servicing in house, your cost structure is different.

This matters when you make decisions on keeping and selling servicing.

If it’s cheaper to use sub-servicing, then you may make your hold/sell choices differently.

Investors look closely at publicly traded IMBs to see if they’re hedging or not hedging.

Banks are mostly always hedging because they aren’t as cash constrained as IMBs.

IMBs hedge about 70% of cap if they do hedge, and banks are higher.

Mortgage Servicing Strategy – Part 3

How does recapture impact performance?

To answer, you have to define refi or purchase recapture.

And you also have to define loan types.

For example, an FHA purchase recapture will be higher (because it’s ostensibly easier to retain).

But conforming refi recapture might be lower because it’s more competitive.

THE BASIS POINT NOTE

This is where servicer tech to help engage borrowers better is critical.

There are much different tactics for refi vs. purchase recapture.

For refi, you have to be reminding borrower of your value to them all the time.

For purchase, you have to make sure your borrower is thinking of you — their servicer — when they start to think about buying a new home. This is arguably harder.

Nuance on cap markets vs. salesforce for recapture:

Cap markets teams would rather originate that retained loan through an internal team because it’s cheaper commission paid.

Salesforce would rather retain that loan themselves and getting paid well to do so. They also might be better at retaining it, but they do it more expensively for the company.

Mortgage Servicing Strategies – Part 4

Insurance and taxes are going up, so servicers get hammered by borrower questions on why their payment went up.

This is complicated from a customer service standpoint because borrowers don’t get that taxes and or insurance go up and have nothing to do with their mortgage payment which is fixed.

They just know it’s payment shock.

This is the source of thousands of CFPB consumer complaints.

Key thing to watch in 2023-2024 FHA pools:

When rates drop and refis come, watch closely who doesn’t refi. These folks might not refi because they can’t, which means they might default.

Sell your Ginnie Mae servicing now?!

While valuations are still attractive and the loans are still performing?

As for servicing costs, the tech stack is more expensive than sometimes shows up in MBA cost analysis.

The tech teams required to upkeep all the changes is a cost that’s often not counted.

Economic, fair, and trading values of servicing are 3 different numbers.

Tech absolutely impacts these numbers.

MBA strategy & team is so tight, they even dress the same!

MBA CEO Bob Broeksmit (right), Chairman Mark Jones (left), and their whole team are at the top of their game.

The job of the MBA is to ensure a safe and sustainable real estate finance system for the benefit of American consumers.

To serve the best interest of consumers means aligning the interests of banks, lenders, servicers, regulators, policymakers, GSEs, private investors, fintech firms, and all other multivariate participants in the housing economy.

This requires understanding of every nuance on how Wall Street, Main Street, Washington, and Silicon Valley all work together.

No small feat, and needless to say, it requires a tight team.

And these two — Mark and Bob — are so damn tight, they showed up at one of the final events here in NYC wearing the same outfit, LOL!

Love it.

Good Night Times Square. Good Night MBA Secondary 2024.

Great run for our industry in NYC.

It’s been a very rocky couple years as the Fed inflation fight deeply impacts the rate sensitive housing economy.

But the Fed’s dual mandate of full employment AND price stability requires rough patches like this.

But the system is stable.

And like CFPB Director Rohit Chopra — the top consumer finance regulator in America — said twice publicly on stage here at MBA Secondary:

The mortgage industry is the adult in the room in the financial services industry that the CFPB oversees.

This is a strong, hard-earned moment for our industry.

Thanks to the MBA Secondary 2024 team for a great end to the Spring conference circuit.

And special shout to Dawn Williams and her amazing team for impeccable production on this and all MBA shows.

That’s it for The Basis Point Live Blog at MBA Secondary 2024.

Hope it was helpful if you missed the show, or if you were here but in meetings the whole time.

Cheers, thanks for reading.