WeeklyBasis: Rates May Go Lower Still (CHART)

Rates ended last week down .125% and back to record lows: 30yr single family home loans to $417k closed at 3.625%. Here are rates for all loan tiers.

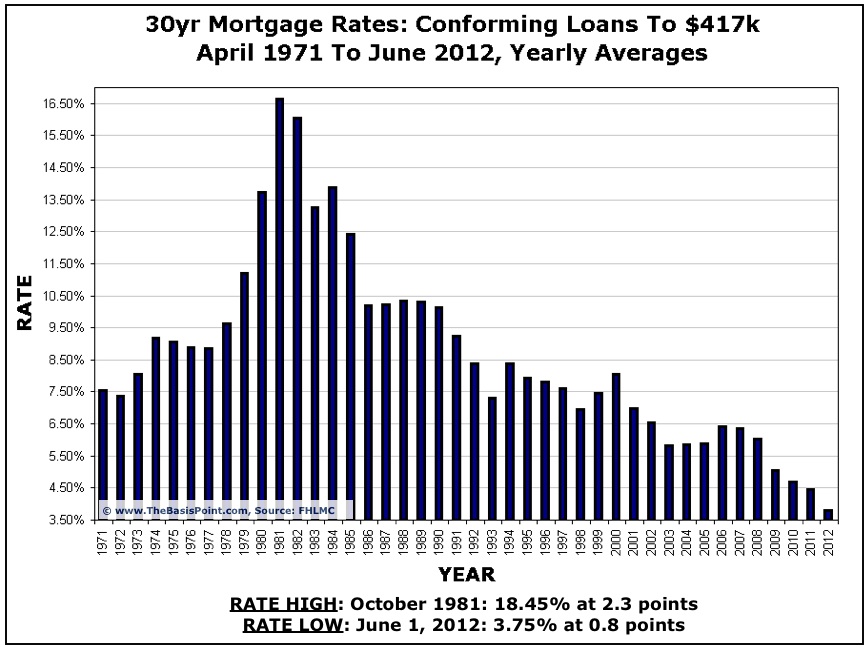

In the chart above (FULL SIZE), the 2012 bar is yearly average through today, which is 3.89% with 0.78 in points. Points are fees as a percentage of loan amount used to “buy the rate down,” and are on top of normal closing costs associated with a loan transaction.

{kind=link}

The chart shows a rate low of 3.75%, a bit higher than the 3.625% in my opening line, because the chart uses national Freddie Mac averages, and Freddie rates are often higher than Fannie rates. The chart’s rates are for loans to $417k on owner-occupied single family homes with at least 20% equity and perfect credit.

The same thing is going on with high-balance conforming loans to $625k. This loan tier is about .25% higher, so 30yr loans up to $625k closed Friday at 3.875%.

These first two tiers of conforming loans react in realtime to trading in bonds backed by Fannie Mae and Freddie Mac loans. These “agency” mortgage bonds (MBS) have been considered one of the safest places for global investors to put money since 2008, and especially in the past six weeks as Europe melts down and U.S. economic growth slows and our job market struggles.

In fact, agency MBS levels suggest rates on loans to $625k should be even lower, but lenders so far aren’t passing lower rates to consumers until they see if this MBS rally can sustain itself—rates drop when bond prices rise on rallies.

As for jumbo loans above $625k, they’re not subject to every whim of MBS trading because jumbos aren’t securitized. Unless you consider five jumbo offerings totaling $1.6b since 2008 a market for securitization. To put that in perspective, jumbo securitization peaked at $1.2t in each of 2005 and 2006. As such, jumbos are priced by lenders individually. They take some cues from an overall low rate market, but mostly it’s lender discretion.

Regarding the overall rate market, the 10yr Treasury Note yield serves as a proxy for that. It closed Friday at an all time record low of 1.45% as global investors also piled into 10yr Notes. This record low goes back 220 years (CHART).

Looking ahead here in the U.S., we’ve got more fiscal brinksmanship coming just like last year when politicians fought so long over the U.S. budget, they got our nation downgraded by S&P.

Ironically a downgrade of our debt caused more global investors to buy our debt because it continues to be the least bad option. And that theme is still the same with Europe’s debt troubles far worse than ours, and a series of critical EU events coming aren’t likely to provide much resolution. It’s going to be a slog there.

The result will be sustained low U.S. rates. How low is hard to tell. We’d been holding 9 months for 10yr yields this low, and just hit the target Friday.

And as noted above, a little time needs to pass to see if the MBS rally can sustain itself. For now, the territory we’re in is literally uncharted, so a bit more time needs to pass for technical (chart) analysis to reveal some signals.

So enjoy the lows for now. They’re some of the only good news in a rather grim global economy.