WeeklyBasis 7/3/2010: Off-The-Charts Low Rates (CHART)

Rate Snapshot

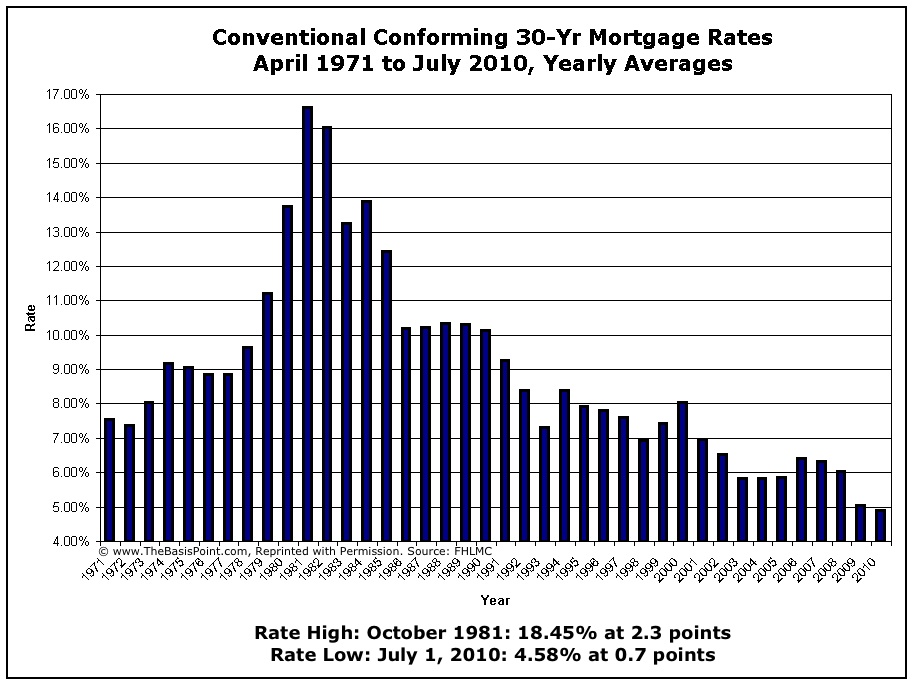

Rates have dropped steadily since May 6 and hit two new record lows in each of the last two weeks. Rates for Conforming loans up to $417k, Super Conforming loans $417k-729k by county, FHA loans, and jumbo loans above $729k are below. Here is a chart showing Conventional (non FHA) 30yr Fixed mortgage rates from 1971 to Present (FULL SIZE CHART). The all-time record low of 4.58% with .7% in points was set the week ending July 1. Here’s the fine print on rates used in the chart. The fine print on the rates in this WeeklyBasis report is at the bottom of the report.

Rates have dropped steadily since May 6 and hit two new record lows in each of the last two weeks. Rates for Conforming loans up to $417k, Super Conforming loans $417k-729k by county, FHA loans, and jumbo loans above $729k are below. Here is a chart showing Conventional (non FHA) 30yr Fixed mortgage rates from 1971 to Present (FULL SIZE CHART). The all-time record low of 4.58% with .7% in points was set the week ending July 1. Here’s the fine print on rates used in the chart. The fine print on the rates in this WeeklyBasis report is at the bottom of the report.

{kind=link}

Why Rates Are So Low

In an unprecedented rate stimulus exercise from January 1, 2009 through March 31, 2010, the Federal Reserve bought $1.25 trillion in mortgage bonds. Rates are tied directly to mortgage bonds, so when those bond prices rise on buying rallies, yields (or rates) drop. Rates were already near all-time lows as of March 31 when the Fed ended its program.

Then a month later on May 6, Greek parliament voted on austerity measures to increase taxes and cut spending (including wage cuts for about 20% of their workforce), and rioting ensued. That caused a brief 1000 point drop in the U.S.’s Dow stock index, and despite recovering from lows that day, stocks (again using the Dow as a benchmark) have lost 1240 points, or 11.35%. European bonds have taken big losses as the debt crisis spread beyond Greece. And here in the U.S., weaker new and existing homes data in the past 2 months, and June’s weak employment report has also caused market participants to question the strength of the economic recovery.

The end result is heavy buying of Treasury bonds and mortgage bonds since they’re both considered the safest investments relative to other options globally. Mortgage bonds have steadily risen from Fed-induced March 31 highs to staggering new heights, which is why rates are down.

Rate Lock Bias Continues

This report has maintained a rate lock bias since mid-May for current homebuyers and for homeowners who have borrower AND property profiles that qualify for refinancing. It seems improbable that current levels of mortgage bonds can hold, and if they break lower, rates will rise. There are no economic reports of particular note for the holiday shortened week beginning Tuesday, July 6.

Hope everyone has a wonderful Independence Day Weekend…

Daily Consumer-Friendly Commentary

In addition to this WeeklyBasis report, you can get daily updates by following The Basis Point’s Twitter feed at www.twitter.com/thebasispoint and/or you can ‘Like’ www.facebook.com/thebasispoint and headlines will flow into your Facebook stream.

CONFORMING RATES ($200,000 – $417,000) – 0 POINT

30 Year: 4.625% (4.74% APR)

FHA 30 Year: 4.75% (4.89% APR)

5/1 ARM: 3.5% (3.62% APR)

SUPER-CONFORMING RATES ($417,001 to $729,750 cap by county) – 0 POINT

30 Year: 4.875% (4.99% APR)

FHA 30 Year: 4.75% (4.88% APR)

5/1 ARM: 3.875% (3.99% APR)

JUMBO RATES ($729,751 – $2,00,000) – 1 POINT

30 Year: 5.375% (5.49% APR)

5/1 ARM: 4.25% (4.37% APR)