LIVE BLOG: Goldman Sachs Housing & Consumer Finance Conference 2022

Hey folks, it’s time to live blog the Goldman Sachs Housing & Consumer Finance Conference 2022!

This is ground zero for banks, lenders, and fintech software firms to meet about how to make homebuying, banking, and personal finance overall easier and cooler for you.

This fast-paced day — and live blog — includes important notes on the economic outlook and hot new finance and real estate trends Goldman Sachs and other major global investors are betting on.

It was 2019 the last time this summit was live. It was all set to go live in March 2020, was cancelled the night before due to pandemic market chaos, and national lockdowns began a week later.

There’s certainly a different type of market chaos today.

Both stocks and bonds have been selling all year as the Fed battles inflation, and this week has been particularly volatile. The bond selloff this year has caused a rate spike, which adds more expensive loans to other rising consumer prices.

The Basis Point’s live blog will include details on how this might play out. This is a very smart crowd, and everyone’s here to better serve consumers.

So let’s get to it, and please reach out to connect directly.

Goldman Sachs Housing & Consumer Finance Conference Table Of Contents

- A Special Shout To Goldman Sachs From The Basis Point

- From Mostly Refis To Mostly Purchases In 2022 Mortgage Market

- The Quiet Before The Live Blogging Storm

- Goldman Research Team Kicks Off With Inflation Themes & Predictions

- Is Fed Quantitative Easing Permanent Now?

- Fed Restoring Credibility On Inflation

- Supply Chain Issues & Inflation Impact

- Optimizing Consumer Experience In Banking & Credit Cards

- Next Gen Consumer Loan Underwriting & Approvals, and Market Strategies

- Which Mortgages Do Investors Like To Buy Right Now and Why?

- How Opendoor, Divvy, Pretium Are Helping Homebuyers – rundown of each of their strategies

- Real-Time Mortgage & Consumer Finance Innovation – with Mike Cagney of Figure/SoFi & Sam Schey of Rocket

- Emerging Consumer Finance Products with Ramp and LendingPoint

- Mortgage Originations In A Tough Market – with HomePoint, United Wholesale, NewRez/Caliber, CoreVest

- The Path Forward For Consumer Credit – with LendBuzz, Mercury Financial, Genesis Financial

- State of Mortgage Servicing In 2022 Rising Rate Cycle – with Mr. Cooper, Annaly, Two Harbors

- The Basis Point Live Blog From Goldman HQ Is A Wrap – for now…

A Special Shout To Goldman Sachs From The Basis Point

I first must thank the Goldman team for including The Basis Point in this summit in recent years. It’s great to be back, and we humbly offer our Goldman HQ fan art here to mark the occasion…

I can’t wait to see how 2022 trends compare to trends from our 2019 Goldman Sachs Housing & Consumer Finance Conference Live Blog.

Things were going well in mortgage then, and then the pandemic helped deliver two of the best years ever for the industry.

Now higher rates and acute homebuyer strain make the situation different.

Still lots of opportunity for lenders, banks, and software firms who power them. Especially if they can prove resilient between now and next year, when Goldman expects inflation to moderate.

In addition to the 2019 Live Blog, we also did a roundup of 15 Things You Need To Know About Banking & Homebuying from Goldman Sachs.

From that, there are 3 things I want to revisit here before we kick off the 2022 conference.

First, we mentioned how your loan servicer will get hip and digital. Sure enough, mortgage servicing is red hot in 2022 with two landmark software deals in this space — Sagent/Mr. Cooper and ICE/Black Knight.

Second, we noted how Wall Street would continue buying more homes. This trend has continued, giving consumer buyers one more party to compete with.

Third, there was evidence of a housing market power shift from sellers to buyers. The pandemic gave sellers even more power, and it’s still all bidding wars and rising rates for homebuyers. But today we’ll hear more on potential buyer relief.

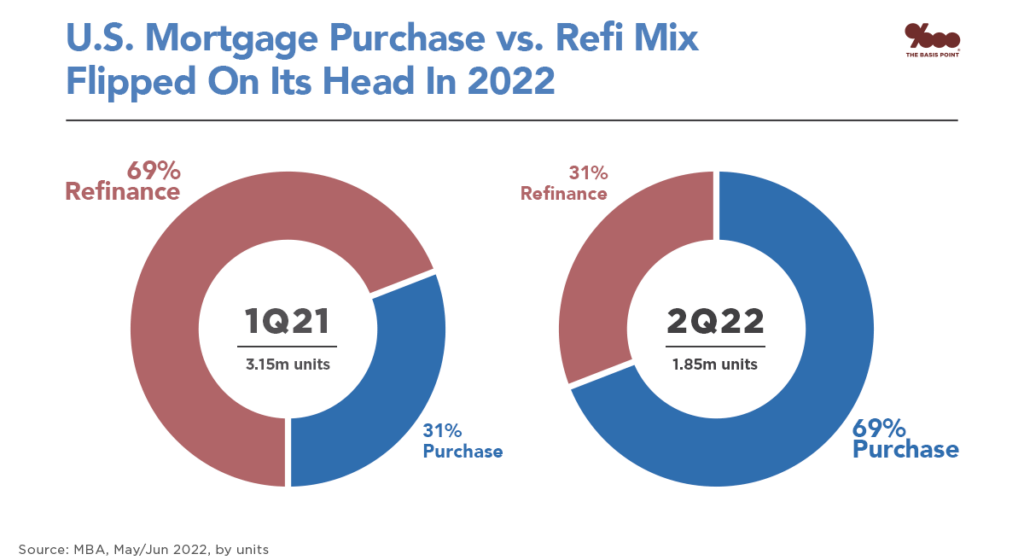

From Mostly Refis To Mostly Purchases In 2022 Mortgage Market

The chart below shows how starkly the mortgage market has shifted from refinance loans to home purchase loans from the beginning of last year till now.

This is 1Q21 compared to 2Q22.

If we look compare the full year 2022 to 2021, purchase loans remain reasonably consistent despite refis dropping sharply.

Lenders made 4.8m loans to consumers buying homes last year.

And this year, the number holds pretty steady at 4.48m.

If the Fed’s inflation fight works and rates come down a bit, this number would improve.

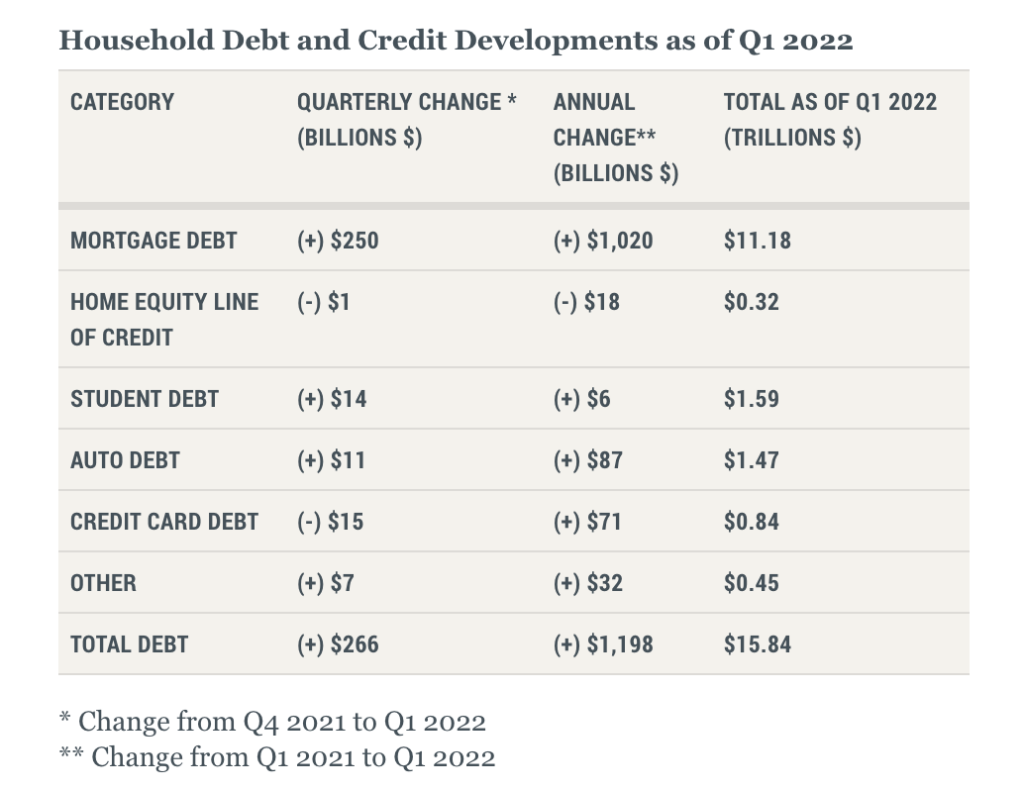

Today’s topics will also cover the consumer debt picture. To put that in perspective, here’s the Fed’s latest stats on debt levels of consumers across all of their key debt categories.

Mortgage debt grew $250b in 1Q22.

Student and auto debt grew $14b and $11b respectively.

But credit card debt declined $15b in 1Q21.

This Goldman Sachs Housing & Consumer Finance Conference has a few key segments on credit cards.

Stay tuned…

The Quiet Before The Live Blogging Storm

Getting ready to kick off…

Goldman Research Team Kicks Off With Inflation Themes & Predictions

[Note: “we” is various Goldman panelists unless specifically noted who said it]

Zach Pandl said we’ve peaked in mid-8% range inflation and we’ll come back down materially by end of next year.

We’ve already seen inflation come down a bit and we think it’s peaked.

You’ll see a material decline in consumer spending this year.

Stimulus from 2020-21 is gone and Fed is raising rates to slow inflation.

As for recession risk, it seems probably but unlikely when you’re adding almost half a million jobs per month.

It’s about 35% probability of recession next couple years.

Ronnie Walker said market is certainly pricing in a higher probability of recession.

But until we move beyond retail and tech on this stock correction and it’s sustained (beyond this week), then this probability grows.

Lofti Karoui said that long/short and derivatives trading signals more recession signals, especially in recent weeks.

Bond volumes are down meaningfully but is about issuers not wanting to come into the market, which can signal recessionary behavior.

Flashing yellow for now, not red yet.

Have we seen a peak in bond yields (aka rates)?

At front end of curve, market has priced for very aggressive Fed hike cycle.

So a lot is priced in.

Now we’re beginning to see weakness in economy.

This is normal. This is the Fed’s goal. This is how you quell inflation. You must slow demand.

[JULIAN NOTE]: This is a critical, counterintuitive point that you don’t hear in all the media hysteria. Read that line above again.

The long end of the curve is determined in global context (vs. short end being more Fed-determined).

Long rates have risen partly because Europe rates rising. This reduces demand for U.S. debt like Treasuries.

We think 3.30% is end of year target for 30yr Treasuries.

Relative to your normal rate hike cycle, this one hasn’t been well digested.

You went into the year with a sharp 2% rate spike.

The agency MBS bond market is where you had a direct subsidy from government.

It’s supposed to do well in a bear market.

But rates are rising despite bear mood for stocks.

Will the Fed become an outright seller of MBS like many think?

[JULIAN NOTE]: This might not happen if you look at what NY Fed chief John Williams told our MBA conference a few days ago. My tweet thread below describes the nuance between letting MBS run off Fed balance sheet vs. outright MBS selling by Fed.

1/ @NewYorkFed head John Williams at MBA Conf today

Inflation too high above our 2% target

This means higher rates to bring down inflation

3 goals from May FOMC meeting

1. Hike rates to get to more normal levels

2. more hikes to come

3. plans to reduce Fed balance sheet pic.twitter.com/PIKoz9vcF4— Julian Hebron (@TheBasisPoint) May 16, 2022

If you set aside the risk of Fed selling outright (which Williams said is unlikely) this rate spike from MBS selloff should moderate.

WILL WE SEE HOUSING SLOWDOWN?

Affordability is now at 2005 levels.

Mortgage costs up sharply since last year because of rates and home prices both increasing.

We think housing demand drops off in 2022.

But in 2023 we may get back to a more normal phase of housing affordability.

But you can’t talk about tight housing without talking about underinvestment in new supply.

Who is the buyer in the market based on affordability?

This does mean Wall Street buyers can take up some of the demand drop.

[JULIAN NOTE]: This will create lots of headline chaos, but it’s worth considering whether it’s actually productive in supporting a down market if Wall Street buys more homes during a phase like this. More thoughts on this in future posts.

Home price appreciation and mortgage rates are the two primary considerations pushing people from home buying to renting.

This actually drives up rents.

When the pandemic happened, mortgage rates went to 3% and less.

Rates are now 2.5% higher, and mobility of consumers is going to be less.

There is a lot of stock of unfinished homes in the economy.

The things that push prices for homes is going ever higher now.

But if you look at the points above, it means housing could moderate.

WHERE ARE WE IN THE CONSUMER CYCLE?

From an income perspective, it’s not great for consumers this year.

The Fed is trying to moderate this with rate hikes.

This is necessary to quell demand in an overheated economy.

But [JULIAN NOTE] consumers HATE this and it’ll cause a lot of unhappiness.

Not everyone had a ton of pent up savings. Some did, but not everyone.

We had a sharp increase in credit card prices at the end of march (which is different from the 1Q22 credit card balance decrease data above)

Tremendous policy support has helped consumers, but it’s waning now.

The strength of household balance sheets is good for a soft landing on the recession scenarios.

It is running out, but it has helped.

KEY TAKEAWAY: Households (and businesses) are decently positioned for higher rates and intentional Fed-induced slowing of demand.

But the lower end of consumer feels the impact immediately of any price increases and other economic strain.

Will see delinquencies rise a bit (late payments on debt), but nothing that’s ringing loud alarm bells now.

WILL WEALTH EFFECT OF LOWER STOCKS & CRYPTO IMPACT CONSUMER SPENDING?

As an asset class crypto isn’t enough to move the broader economy.

The interconnectedness and size of that market is too low to have a crypto correction impact the economy.

RISKS GOING FORWARD

Housing and consumer spending have very meaningful impacts on economy.

We do believe that labor would weaken and inflation could be more persistent into next year.

But for now we haven’t materially changed our models that say the Fed will succeed in bringing inflation down.

What this means is the U.S. consumer will look weaker in the face of higher prices, and less government stimulus checks.

The U.S. economy will look weaker.

This is part of the process.

Another consideration is a European recession because of the war, and a China recession because of COVID lockdowns.

Both of these could pose worse risk in the U.S.

On the company profit side: the pre-pandemic world was all about top line growth, now it’s all about margins.

This is one of the reasons stocks are getting hit hard.

Is Fed Quantitative Easing Permanent Now?

Regarding quantitative easing (QE) from Fed (when they buy bonds to keep rates low), is this permanent now?

In short yes.

The flip side of it is QT — quantitative tightening — which is when the Fed sells outright.

[JULIAN NOTE]: Again, the NY Fed said they’re not going to sell outright.

1/ @NewYorkFed head John Williams at MBA Conf today

Inflation too high above our 2% target

This means higher rates to bring down inflation

3 goals from May FOMC meeting

1. Hike rates to get to more normal levels

2. more hikes to come

3. plans to reduce Fed balance sheet pic.twitter.com/PIKoz9vcF4— Julian Hebron (@TheBasisPoint) May 16, 2022

But if the market fears QT that’s sometimes just as bad. The market will sell bonds and ask questions later.

Fed Restoring Credibility On Inflation

The question isn’t so much whether the Fed gets back to their 2% Core PCE inflation target.

It’s how aggressively they’re going to try to get there.

Also worth noting central banks globally are getting more comfortable with slightly higher inflation. More stimulus.

It used to be only Fed inflation hawks went to heaven.

That’s changed now.

Long term inflation expectations look to be coming under control.

But this new willingness to let inflation run to help consumers does create short-term uncertainty, especially for small businesses and consumers.

Eventually long-term and short-term expectations for inflation will converge and get to the 2% range.

Not without some short term pain.

Supply Chain Issues & Inflation Impact

You can’t reply to a supply shock in same way you reply to a demand shock.

Fed has chosen to address demand side rather than supply side.

Demand side is slowing economy, which means slowing demand.

[JULIAN NOTE]: I don’t think consumers get this.

They don’t want inflation but they also don’t want the medicine that it takes to quell inflation.

Optimizing Consumer Experience In Banking & Credit Cards

Next up at Goldman Sachs Housing & Consumer Finance Conference…

This panel is three consumer finance companies — Mission Lane, Aqua, Cardworks — that each have a special sauce on how to serve consumers with banking and credit card products.

How do you do credit cards in a mission-driven way?

Mission Lane: It’s about giving folks who don’t usually get credit — or have a tough time getting it — like a prime credit customer. They need immediate and easy access to credit.

Aqua: they enable financing through dealers. So if you’re buying a water toy or doing home improvement, they’re the ones who give those dealers or contractors the ability to finance you for those purchases.

Cardworks: Our job is to get credit costs down. We focus on these 4 things:

– Better product, terms, policies

– Better digital experiences. Actually enjoyable.

– Better agent experiences: when you have to talk to someone, do they solve your issue

– Better community and treatment. Are you just a customer or do you feel like you’re involved in some way.

Dan Pillemer at Cardworks made a good point about the MUST for catering to different customers.

There are the customers who call and need to talk with reps for hours.

And there are customers who’d NEVER talk to reps, and must do everything online.

These experiences must be covered equally well.

+++

Rich Morrin said it’s not about tech first, it’s about people processes first.

First you musts train people how to handle basic customer inquiries about balances or complex conversations like collections.

He spends 90% of his time working on these things. They’re more important for customers, they’re harder, and they’re core to the business.

Then the technologies can be built around this.

Henry Domenici at Mission Lane agreed with this, adding that if the technology does too much, your customer support folks don’t know enough.

[JULIAN NOTE]: It’s refreshing to hear boutique companies like this put such high value on team member expertise. I agree this is key for building credibility with customers.

+++

Henry/Mission Lane: The fundamentals of customer needs hasn’t changed, but the way people use credit has.

Example: much less use of cash means higher card use volumes.

Rich/Aqua: During pandemic, you really need to talk to people more because of hardships consumers are going through.

This was when we really focused in on training our folks to being empathetic during a tough time for consumers.

It was complicated. We didn’t know how lenient to be during hardships and whether the economy would recover (this was early in pandemic).

So we spent most of our time on training.

Then we realized our tech was too old, and made material tech investments in 2021 to upgrade the tech.

+++

Dan/Cardworks: live chat is one of the most effective tech tools they use.

This is what drives self serve.

Collections are different and more phone driven given sensitivities, but live chat is still the fastest path to humanize contact.

Henry/Mission Lane: there’s no shame in partnering with fintechs to power your operations.

There’s danger in building everything yourself. Things change too fast.

Rich/Aquq: we don’t use as much fintech for evaluating customer sentiment because we use our people to monitor that.

Dan/Cardworks: allowing self-serve on disputing charges drives both operational efficiency and customer satisfaction, but there are still big human elements on this.

+++

As we get into a recessionary environment and consumers are more strained, the customer service is all the more critical.

Notable: Cardworks average monthly payment is $50.

Henry/Mission Lane: getting customers to like you makes all the difference.

We enabled hardship programs online and this helped a lot of folks navigate the pandemic phase.

+++

Rich/Aqua: we have data on each customer so we can engage well with proper staff.

We’re not using that data as well as we want to just yet.

That’s where the maturing tech strategy will help.

+++

MARKET OUTLOOKS

Rich/Aqua: My baseline is always nervous, and we’re in for some pain this year.

Budgets are getting stretched meaningfully.

There’s no evidence the Fed will get us to a soft landing.

So we think strain will be in consumers’ lives for awhile.

Even with strain, our goal is to make sure we can help people stay on time with payments.

This is our core consumer experience focus this year, and it comes down to training and empathy.

+++

Henry/Mission Lane: We do think our models on repayment aren’t quite accurate given market movement now.

Hence we have to be nimble.

That’s the main goal.

+++

Dan/Cardworks: We’re legitimately scared on how this will play out for the consumer.

The ability to look at early indicators like fraud claims is one example of seeing how repayments might happen.

Consumers sometimes test waters of not paying, and we’re watching that very closely.

“WINTER IS COMING”

Dan/Cardworks said this Game of Thrones quote to summarize his firm’s view of the short-term.

[JULIAN NOTE]: This Game Of Thrones market outlook is a key indicator for the short term.

If the previous session was about a decent scenario emerging by second half of 2023 — Fed inflation battle works — then this session was about the reality on the ground now.

And the reality is consumers will feel some strain, as these boutique credit firms just laid out.

Next Gen Consumer Loan Underwriting & Approvals, and Market Strategies

Next up at Goldman Sachs Housing Consumer Finance Conference…

This panel is about how to enhance human loan approvals and, where possible, fully automate loan approvals.

This is more common outside mortgage, and this is what this panel will explore.

Jason Gross/Petal is machine learning/AI native. They can instantly assess income volatility, view expenses, debt, and other fixed obligations that act like debt — like utility bills, etc.

A lot of people talk about machine learning as a buzzword, but we actually use it.

We started leveraging aggregated consumer data.

Pulled in data from companies that sit between lenders and consumers.

Bank account data isn’t like credit reports, which are structured.

But we make sense and process stuff that doesn’t make sense.

We pull payments off of bank statements as an example, so we can see what people pay in rent and other bills that don’t show on credit reports.

There are 10,000 attributes.

Of these, we zoom in on the ones that are important for making lending decisions.

We also build in all the consumer privacy and compliance so we can tell a consumer why they were or weren’t approved.

We issue an underwriting score that helps to make loan approval decisions.

Today our cash-flow underwriting decisions are better than credit bureau data.

Then if you combine them, you get a 30% lift over bureau models.

We can drive a significant lending decision.

For now it’s focused on smaller loans, but it’ll be applied to all credit types within 5 years.

+++

Mark McCall/Global Lending Services focuses a lot on auto lending.

Our analytics, credit policies, and pricing must align to market.

We started in 2012, and have since signed up 12,500 car dealerships.

The growth has been driven by automated underwriting and approvals.

This was the difference between being un-needed and needed by these dealers.

They’re the ones sending applications to us, and we do take turndowns from them.

Example: Nissan will send us a turndown, and if we can tell them in seconds if we can do the loan, they stick with us.

+++

Jason/Petal: We receive applications up and down the credit spectrum.

Here’s what’s interesting about cash flow model — two people with lower credit scores could have drastically different cash flow.

One is a stronger borrower and one isn’t.

But traditional credit-score heavy models are going to view these borrowers as the same.

Consumer cash flows are relevant whether you’re underwriting credit card, personal, student, auto, HELOC, or other forms of credit.

It doesn’t matter whether you’re in Kansas or Kenya. Cash flows are the primary determinant of how people can repay loans.

+++

MAKING LOAN APPROVAL DECISIONS REALTIME

Jason/Petal noted credit reports have 30-day old data, and derogatory data is also even older.

But we can pull in earlier signals because we’re looking at data in real time.

This is especially important in real-time markets.

Pandemic was a good example where folks came under strain right away.

And the same is true now as the market corrects during the Fed’s inflation battle.

+++

OUTLOOK FOR NEXT 6-12 MONTHS

Jason/Petal is looking to add more data sources for making decisions.

Example: want to add Buy Now, Pay Later payments which aren’t on the credit reports yet.

More data, better models, more use cases.

Mark/Global Lending Services is looking to reconcile what current economic bumps are doing to credit profiles.

He was very focused on his models making the best decisions in real-time as this market cycle plays out.

Which Mortgages Do Investors Like To Buy Right Now and Why?

Nancy/MetLife likes whole loan sales, and within that sector non-QM.

For those who don’t know what this means, she likes the market for buying whole loans from mortgage originators (instead of bulk loan pools).

And the kinds of whole loans she likes are loans not backed by Fannie and Freddie.

She likes them now because they’re rigorously underwritten and behave like prime loans even when you’re using bank statements over tax returns to verify income and cash flow (a common approach for non-QM underwriting.

+++

Jason/PIMCO believes we need to reset our expectations from the double digit home price growth we’ve seen.

Within FHA, which is a good loan for folks who are stretching affordability, we’re watching supply of FHA closely to see if it can help support the market.

Especially when affordability gets more challenging and FHA is needed more.

+++

Rick/Radian (a mortgage insurance company) said housing inventory shortage is a major issue.

Housing market is being fueled by first time buyers as millennials age into home buying years.

Just today, 28% of existing home sales were to first time buyers.

We expect down payments to decrease in a market like this.

This is normal in a market cycle like this.

Mortgage underwriting is clean today.

Servicers are doing better job of servicing than in the last cycle.

So if down payments decrease (aka loan-to-value ratios rise), the market can sustain it.

We watch risk factors very closely, but we believe it’s sustainable.

+++

Rick/Radian qualified his points above that we’re not trying to be overly optimistic.

But removing some demand and keeping borrower approval standards — and loan types — clean will make this sustainable while enabling higher LTVs.

Balloon payments, and overly-creative ARMs, and LTVs higher than 100% where what caused the crisis.

This market is nothing like that.

+++

Jason/PIMCO said that most of the non-QM market (meaning mortgages not backed by the government) today vs. early pandemic is much more stable.

This reconciles with Nancy’s opening comments above which were supportive of non-QM loan investing.

[JULIAN NOTE]: FYI, one reason investors like non-QM (when the timing is right, like now) is because they have higher rates, which means higher returns to investors.

+++

“WE’VE BEEN IN THE FIRST INNING OF TECHNOLOGY FOR 20 YEARS”

It still costs $9000 to originate a loan.

Technology is leading the way, but it always takes longer than our industry plans for.

This point was from Rick/Radian.

[JULIAN NOTES]: I love the 20-year first inning comment, and here’s the deal on the cost and tech trends.

Mortgage software powers mortgage lenders to serve consumers, and software is a growing line item in lenders’ per-loan costs, which hit an all-time high of $9470 in 4Q21, per MBA.

These software costs, which doubled in the past 10 years, get passed onto consumers.

The MBA reports that technology costs for large banks rose from 8.3% of total mortgage company costs in 2012 to 15.1% in 1H21. And from 4.8% to 8% for large nonbanks.

The mortgage software modernization wave began in 2012, and the efficiencies of this rewiring of U.S. housing haven’t manifested yet.

+++

FED IS BEHIND THE CURVE, RATES ABOUT PEAK NOW

Nancy said the Fed is playing catch up.

We’re not going to see a massive increase in rates beyond what we’ve seen so far.

Jason said “Don’t Fight The Fed” now that they’re going the other way.

How Opendoor, Divvy, Pretium Are Helping Homebuyers – rundown of each of their strategies

Josh/Pretium said the macro story — rates and home prices rising — is the main theme now, and one of the biggest consumer cost spikes ever in such a short time.

They scour the MLS and buy homes for the purpose of renting them out.

High conviction on housing shortage driving demand for rentals.

Here’s a white paper on Pretium’s housing shortage thesis.

+++

John/Divvy describes his firm as helping renters become homeowners.

We raised $400m on $2b valuation, buying thousands of homes per year.

Before rates started rising, we had customer demand from borrowers who didn’t have savings.

Now that rates have risen, they have customers who want to work with Divvy to save and plan for a purchase in a couple years.

+++

Josh/Pretium said they also help consumers in the same way Divvy does.

They are working with fintech partners to make positive rent payments reflect on credit scores.

This is how most renters with otherwise light credit can get into the market.

+++

Dod/Openoor went from 3.5% to 6% margin by getting operations sharper, not just market movement.

Opendoor buys your home instantly and is the category leader in this iBuyer space.

They’re in 48 markets.

Dod talked about how their ground game is getting tighter all the time.

Example: their inspectors can find property defects like cracked foundations, water intrusion, etc. really fast and at scale.

These physical inspections happen on most individual real estate deals.

But it’s hard to do this at scale, and Opendoor is getting the process down tighter.

+++

John/Divvy is mainly focused on Georgia, Florida, Texas.

These markets have higher cap rates (which is income a property generates divided by property value).

+++

Dod/Opendoor: It’s truly crazy how little innovation has happened in the real estate space.

The one-click home sale vision for Opendoor will take 10-ish more years to polish.

But [JULIAN NOTE] the instant buying Opendoor is doing is very efficient and they’re maturing responsibly. The down market test insiders often ask about is coming, but Opendoor can control this with efficient offer prices — and now they have a good record of selling properties fast. If they buy well, they could in theory sell fast in a tougher market.

We convert 35% of home sellers who ask for an offer.

This is a huge conversion rate.

+++

Josh/Pretium thinks a risk factor is less sellers because they’re locked into great 3% mortgages.

They’re also partnered with homebuilders to solve some of this inventory shortage problem.

+++

Dod/Opendoor: We’re trying to hold homes as short as possible.

We’ve been increasing our discount to account for increase in uncertainty in this market.

Our conversion rate of 35% is with this discounting.

OPENDOOR: We’re not taking 3 year risk on housing. We’re taking 3 month risk on housing.

+++

IS MORTGAGE CREDIT TOO TIGHT OR LOOSE NOW?

Dod/Opendoor: For our business, we think borrowers are ok now, but given our 3-month timelines we have to watch this in real-time and often mortgage credit is a long-term consideration.

John/Divvy: Our goal is to get folks to be able to eventually afford mortgages.

Part of that strategy is to add our own mortgage capability.

Josh/Pretium: To answer the mortgage affordability question — and keep it affordable long-term — we must address the housing inventory issue.

Under-supply of homes is the main issue contributing to affordability.

Cheap debt isn’t the only solution to home affordability. More inventory is the solution.

Real-Time Mortgage & Consumer Finance Innovation – with Mike Cagney of Figure/SoFi & Sam Schey of Rocket

Looking forward to this next session, will be rapid fire. Stay tuned…

Mike/Figure: Figure is a lending, payments, exchange firm that’s all blockchain powered by Provenance blockchain.

+++

Sam/Rocket: Rocket is America’s largest mortgage lender but rapidly transitioning to consumer loans.

Also adding mortgage as a service by powering other firms such as Schwab for mortgage.

+++

Mike/Figure: Blockchain allows you to create digital-native assets that displace trust with truth.

This means all parties from origination to securitization don’t have to keep re-verifying loans.

Then you can create marketplaces that you don’t have to have every single counter-party.

In mortgage, you can bring liquidity and certainty and maybe remove warehouse lenders as an example, connecting originators directly to investors.

The Digital Asset Registration Technologies (DART) that Figure developed enables fully digital eNotes and this is a key last-mile for digital-native mortgages.

+++

Sam/Rocket: Everyone thinks Rocket is a super easy application.

The secret is that it’s origination to close is all streamlined.

Servicing is key for us (and JULIAN NOTE) they have approximately 3X industry average retention.

+++

Mike/Figure: DART is democratization of mortgage by making mortgages tradable on day one vs. 30-60 day windows of due diligence that slow down the originations to securitization process now.

This platform is real-time. Trades happen in real time.

[JULIAN NOTE]: I’ve been close to this story and the industry has come catching up to do on truly understanding that day-one trading is possible. It’s very exciting.

+++

Sam/Rocket: Rocket Homes is another business in the ecosystem that enables pre-approved borrowers to be connected with local realtors.

[JULIAN NOTE]: This was born from a conversion goal within Rocket, but now it’s really changing consumer experience.

+++

Mike/Figure: The USDF initiative Figure/Provenance is running represents fiat currency on the blockchain.

[JULIAN NOTES]: This is different from the crypto-native tokens that crashed recently.

USDF initiative has 25 real banks on board (with 100-ish in pipeline) so it’s all about properly representing fiat currency (aka dollars) on the blockchain.

Blockchain is just the marker for real dollars. This is the key.

Most people think DeFi is the disintermediation of banks, and this is just wrong. Banks are critical.

So if payments are happening on Provenance in USDF, it’s just a proxy for dollars. It’s not crypto funny money. [To clarify, these are JULIAN NOTES]

+++

Sam/Rocket:

Rocket’s lending as a service is now powering the bank you trust and have trusted for generations.

[JULIAN NOTES]: THIS is the next phase of the fintech cycle.

Both of these companies prove their cases in the real world, then bring them out to the market broadly in this way. Figure is doing the same vision, albeit less mature than Rocket.

+++

Sam/Rocket: We’re planning to offer borrowers and realtors a guaranteed close.

We’re carving out balance sheet space to do this in markets that are so hot this is required for borrowers to get into homes vs. cash buyers.

[JULIAN NOTE]: If they do this, it’s better than some of the cash-like offer startup models. Rocket could blow this out.

+++

WHY WOULD BANKS LET ROCKET POWER THEM?

It’s all about protecting the Rocket brand and if a bank is Rocket powered that’s another form of brand building.

+++

Mike/Figure: Early use cases on Home Equity Lines of Credit have saved 60+ days in process and 100 basis points.

The reason is the cutting out of the counter-parties with real-time data methodology described above.

+++

ROCKET & FIGURE ON BEING RARE PROFITABLE COMPANIES

Sam/Rocket: Covered Rocket’s ISMs as a core talent, culture attractor. This is what has build the org the way it is.

[JULIAN NOTES] The ISMs are real, and originally written by Rocket founder Dan Gilbert. As a “corporate values” cynic, I believe Rocket’s ISMs are different because they’re philosophies and ideals. This is easier for folks to get behind than values. Why? Because it’s easier to for individuals to process their own way, whereas values too often feel pushed upon employees.

Mike/Figure: It was all about proving blockchain use cases (using Provenance Blockchain) by having Figure’s real lending and payments businesses be the real-life use cases.

+++

BLOCKCHAIN NOISE IS STARTING TO THIN OUT

Mike/Figure: As noted above, DeFi has been noisy and anti-bank.

But now that’s all thinning out, and we’ll start to see how real-world finance can function on blockchain in a fully regulated way.

Sam/Rocket: Future of mortgage is getting to close mortgages in 5 days, and blockchain must play a role here.

Mike/Figure: The adoption of [Provenance] blockchain may end up happening a lot faster than everyone thinks.

+++

Mike/Figure: More than half of our HELOCs were first lien because people have so much equity.

We also have people who have crypto and want to borrow against it.

[JULIAN NOTES]: So they make the loan and lien both the crypto and the home as collateral.

This is the fine print of the Crypto Mortgage in one phrase.

Emerging Consumer Finance Products with Ramp and LendingPoint

Eric/Ramp: helps companies do expense management and is into nine-figure revenues already.

We want to make business owners more profitable.

+++

LendingPoint: Full spectrum lending ecosystem to businesses.

We’re profitable for last 3 years.

Want to accommodate our business customers whether they’re at point of sale or anywhere in their operations.

+++

Eric/Ramp: Before Ramp, he started a company that enabled people

With Ramp, it’s all about solving workflows that waste time for companies.

How do we stitch all that into services.

Here’s the Ramp site for an overview.

Example use case: Expense reports.

People don’t turn in their receipts. It’s once a month. It’s cumbersome for employees and companies.

Ramp can process and approve transactions within 6 seconds based on companies’ policies.

Another example: Finance teams are using multiple systems to close their books.

Ramp consolidates all of this, and streamlines it.

[JULIAN NOTE]: The more I’m listening to Eric, the more I think The Basis Point needs to look into Ramp. But I actually do love our finance team, so we’ll see what they say, lol.

+++

Tom/LendingPoint: We started in 2015 and there were a couple opportunities:

– Customers were unheard by banks for their lending needs

– As we ramped lending, we say other things our customers were spending money on

So we got into the point of sale (POS).

We acquired a POS company.

And then we needed to rework our warehouse lines and get better at funding our customers.

This POS capability lets our customers offer financing at their point of sale.

+++

Eric/Ramp: In prioritizing, we like to focus on where we have competitive advantage.

Cost of capital, distribution are advantages that large players have.

But they’re slow: 3 months to change a site.

Our advantage is going faster with new product for our customers.

+++

Tom/LendingPoint: We’re seeing fatigue with customers making $40k or less.

We’re doing regional debt-to-income ratios to gauge risk there.

We’re also seeing new product interest areas.

For example: there’s a lot of interest in Home Improvement right now.

+++

ARE LOAN APPROVALS TIGHTENING?

If people need more money right as market conditions are tougher, what does this mean?

Tom/LendingPoint: There’s a slowing down of working capital with our customers.

We’re still seeing a lot of application counts (coming in from things like point of sale).

Our average customer is $85k, and that’s not slowing down.

Most of our numbers are line with pre-pandemic now.

This includes credit quality.

+++

Eric/Ramp: We’re going to see a lot of change in the next few months.

We’re watching to see if more of our product activity goes to payroll or expenses or other products.

+++

WHAT IS NEXT PHASE OF FINTECH GROWTH FROM?

Eric/Ramp: We’ve come so far with fintech that you can be a 60 day old company and put credit cards in people’s hands.

You can be the money.

Or you can be the consumer layer.

Embedded finance or workflows.

[JULIAN NOTES]: I like this framing of the fintech cycle circa 2022. Will do more on this.

+++

PREPARING FOR RISK

Tom/LendingPoint: We’ve gone into the capital markets more to ensure we’ve got capital if markets dry up.

If your asset cycle is about 5 years you have to assume some of those cycles will run twice and you must be prepared for that.

+++

Eric/Ramp: His loan product is 30 day product so it turns over much faster.

Also we raised equity capital when we didn’t need to raise so we can be ready for any unforeseen disruptions and/or capitalize on opportunities.

We’re also very careful about taking risk on things we don’t understand.

+++

WHEN WILL CPI BE BELOW 6%?

Eric/Ramp: Maybe late summer or fall.

Tom/LendingPoint: End of year or beginning of first quarter.

Mortgage Originations In A Tough Market – with HomePoint, United Wholesale, NewRez/Caliber, CoreVest

This is another powerhouse — and incredibly timely, important — panel for the 2022 Goldman Sachs Housing & Consumer Finance Conference.

These are some of the huge lenders, two of which went public (HomePoint and United/UWM) in this cycle.

+++

Baron/NewRez-Caliber: Market is somewhat stressed, but also a return to normalization.

[JULIAN NOTES]: Amen, this is exactly what this market is right now.

We focus on profitability in our originations businesses, and we adjust accordingly in market cycles.

We own lots of MSRs, and we acquire them in a very efficient manner.

We look at our correspondent originations business as an MSR acquisition business.

We also want to grow our non-QM business.

Overall we have 3.2 million borrowers in our servicing portfolio.

We also have direct and retail businesses.

Across all of this, it’s not about being number one. It’s about being profitable.

Our servicing business (and also large sub-servicing business Shellpoint) is also a big source of stability, profitability balance, and growth.

+++

Beth/CoreVest: We have sticky products at the short end and long end of the yield curve.

We don’t need to be number one either. We just want to create great assets (aka loans).

For the types of loans we do, there’s no credit issue, but there’ a volume normalization issue.

We balance sheet our loans.

+++

Alex/UWM: The broker will win in a rising rate environment.

We like to think about what’s right for the consumer.

1Q22 was the largest purchase market quarter in 36 year history of UWM.

We like rising rates for this reason: it makes it a purchase market and we’re ready for this because of our broker expertise.

+++

Willie/HomePoint: In 2018 the HMDA (home mortgage disclosure act) data told us that consumers get a better deal through brokers than retail lender.

Then we went all in on wholesale.

Brokers know what’s happening on the ground in local communities with consumers and realtors.

This is the best place for consumers to get a loan because of the advice and the connection to the local community.

+++

Alex/UWM: We view each broker shop we power as small local business.

Broker branches are 4-5 person shops that plug into our model and we do all the business infrastructure for them.

It’s not UWM branding. It’s about the local broker white labeling our software and tools as their own.

[JULIAN NOTES]: This is the power of the modern mortgage broker model. Brokers are fiercely independent and have earned their own local market credibility. They’re the brand. So they need the infrastructure of a great wholesale partner such as UWM or HomePoint to make their own brands shine.

+++

MORTGAGE PRODUCT PRIORITIES RIGHT NOW

Willie/HomePoint: Right now we’re looking at products to help our salesforces.

Example: Partnering to give our brokers the ability to do pre-approvals that are cash-like.

+++

Beth/CoreVest: We like short-term stay loans.

Build-to-rent loans.

Some of our products wind up as owner-occupied homes, but mostly it’s ending up as rentals.

Also: How do we help people unlock home equity. Not HELOCs but more like shared appreciation.

As people get locked into low rates, how can you let people tap equity.

Shared appreciation is a way to do it.

[JULIAN NOTES]: For a primer on shared appreciation, read this.

+++

Baron/NewRez-Caliber: If I’m making 2nd lien credit, I’m watching their first lien very closely, and the property.

This 2nd lien (as a HELOC) product is a big priority for us.

[JULIAN NOTES]: I like this strategy because a a HELOC makes the customer stickier since it’s revolving. It’ll be all about the pricing and the ease/speed of underwriting to see how well it performs. Slow and expensive HELOCs made them unpopular for consumers in the long cycle to this point. But if people are locked into their low first mortgages, now HELOC price premiums will make more sense.

+++

Alex/UWM: We’re closing 40k loans a month and doing many of them in 15 days.

This is how we think about capital.

Faster loans means faster warehouse turn, lower costs, etc.

+++

MORTGAGE RISK OUTLOOK FOR 2022

Baron/NewRez-Caliber: We talk about risk Every Day.

In a mortgage origination context, it’s about operational, consumer, regulatory, and compliance risk.

We go through them all every day.

Our core focus is operational excellence across originations and servicing.

It’s not a secondary topic, it’s the number one topic all the time, 7 days a week.

+++

Willie/HomePoint: We’ve simplified the company to manage for this higher rate, lower margin environment.

We’ve been prepping for this since last year.

Liquidity is our primary focus so we can handle any market shocks that may come.

It’s going to take longer in this cycle for mortgage originators.

We’ve adjusted sharply but others haven’t and it’ll take a couple quarters.

+++

Alex/UWM: We’re always on offense and driving market share.

If the market is $3 trillion and we have 20% of the market in wholesale, and we have 40% of the wholesale market, we’re doing pretty well.

That’s how we think.

[JULAN NOTES]: To clarify, here’s the actual size of mortgage market right now: The market was $3.9 trillion last year and $4.1 trillion in 2020 (a pandemic anomaly) and it’ll be $2.5 trillion this year and $2.3 trillion next year, per MBA — this is more normal. The wholesale market share isn’t 20% right now, it’s 15.3% as of 4Q21, per IMF. The 1Q22 number comes out very soon. But the point is taken: UWM is on offense growing market share in wholesale, and they’re very good at playing offense.

+++

Baron/NewRez-Caliber: The Fed will need to continue to fight inflation, period.

This fight makes homes less affordable.

This will slow down home demand.

The market will be significantly smaller than last year. [JULIAN NOTES]: see my stats above on this.

The Path Forward For Consumer Credit – with LendBuzz, Mercury Financial, Genesis Financial

Amitay/LendBuzz: Car financing platform for 500 car dealerships. We like to focus on folks who don’t have enough credit yet. We have many with no credit yet, and about half with credit of 600-720.

Jim/Mercury Financial: Getting underserved folks into credit cards, then growing those relationships as those people’s financial lives mature. Mission driven.

Bruce/Genesis Financial: Also providing access to credit in some of the nation’s largest retailers and also direct consumer credit to about 5 million underserved consumers.

+++

Amitay/LendBuzz: We will rotate dealerships based on performance of their consumer profiles.

Bruce/Genesis: We’ve seen credit get weaker lately, but we have short cycles, so it’s a constant review of how borrowers are doing.

Jim/Mercury: A lot of big banks have pulled out of serving who we serve, so we like the space.

We’ve noticed that our consumers are very resilient and they want to do the right thing.

We haven’t seen deterioration of repayments yet.

The gig economy makes consumers we serve resilient and most underwriting models don’t catch this.

But we do.

+++

Bruce/Genesis: We have a cautious stance given the proportions of our customers’ incomes that go to basics like food.

So we do smaller balances.

But we agree with Jim/Mercury that consumers are resilient and want to do the right thing.

+++

Jim/Mercury: Inflation is very real for our customers.

When I was running consumer at TD Bank, we saw gas prices where a big reason for people running over credit limits.

This is a factor that’s biting more out of salary for lots of folks now.

We’re watching to see if people have to choose between on-time auto vs. credit card payments.

+++

Bruce/Genesis: We generally underwrite to willingness to repay.

Our customers want and need cars, and are therefore willing to pay.

Jim/Mercury: The car became necessary for our customers during the pandemic.

+++

Amitay/LendBuzz: We’re watching wage and gas expenses, which are very real now.

Our underwriting is based strongly on cash balances.

Approved loans have 50-60% larger cash balances than on the loans we’re not approving.

+++

Jim/Mercury: UDAAP is a regulatory priority for CFBP director Chopra, and we watch this compliance very closely.

We’ve built our org to the very top level of compliance control.

So we feel confident about keeping the consumer safe.

+++

NEW PRODUCT PRIORITIES

Amitay/LendBuzz: We want to come out with new products in next 18 months, but watching market closely before launch.

Jim/Mercury: On the theme of products, we are looking at partnerships that are in demand now.

Airlines and hotels normally do incentives with big banks, but this leaves out a lot of consumers we serve.

Example: Spirit Airlines customers could use more incentives we can help provide with good partnerships.

+++

MAIN TAKEAWAY ON MARKET OUTLOOK

Bruce/Genesis: There’s going to be some noise this year until Fed’s inflation battle plays out with our consumers.

State of Mortgage Servicing In 2022 Rising Rate Cycle – with Mr. Cooper, Annaly, Two Harbors

This is the final session for Goldman Sachs Housing & Consumer Finance Conference 2022, and one of the most important topics in housing this year.

+++

Bill/Two Harbors: Must separate price from value on servicing.

If you didn’t hedge exposure you made money.

We hedged, so we didn’t make a lot recently.

As rates rise, risk and valuation characteristics have changed considerably.

There’s more likelihood that mortgage prepayment speeds slow.

We’re focused on recycling our portfolio into more recent coupons.

+++

Ilker/Annaly: First quarter was good for MSR holders.

+++

Jay/Mr. Cooper: We’ve got $700 billion plus in servicing.

We grew this in the first quarter.

We also want to grow sub-servicing. [JULIAN NOTE]: Two Harbors uses Mr. Cooper for sub-servicing.

+++

Bill/Two Harbors: People can talk about prepayment speeds but data right now is hard to prove most prepayment models.

With higher rates and home prices, with economy leaning closer to recession, prepayment speeds are more on slow rather than fast side.

This means stable servicing values.

+++

Jay/Mr. Cooper: Slower prepayments by borrowers means more opportunities to cross-sell customers.

[JULIAN NOTES]: Cross-sell isn’t a pejorative. It’s looking at customer data and actions and providing them with financial products they’re already looking for. This drives customer retention, and customers aren’t always looking to leave. Mr. Cooper has 2X industry average retention too. So it’s not so much about “cross-sell” as it is about “customer retention” for the right reasons.

Also for non-technical folks reading this, it’s worth noting that higher rates mean loans don’t pay off (“prepayments”) as much, because there’s nothing better to refinance into. So this means lenders can work with you longer. This is what I’m talking about above.

+++

Jay/Mr. Cooper: Technology is our huge priority for mortgage servicing.

We started working with Sagent to make our customer retention strategies and overall servicing better.

[JULIAN NOTES]: Here are details on the landmark Mr. Cooper & Sagent Servicing fintech deal.

+++

Bill/Two Harbors: This inflation fight better work like Paul Volcker told us it would work!

[JULIAN NOTES:] Paul Volcker was the last Fed chief before Jay Powell who had to raise rates sharply to kill inflation, hence the joke. But it’s a serious issue. And hopefully monetary policy and markets overall are more sophisticated now so the Fed can beat inflation by next year instead of causing 2 recessions like it did in the early 1980s.

This market movement has moved so far so fast (JULIAN NOTES: +2.5% on 30yr fixed mortgages for consumers December to present), we have room to get a little better.

The Basis Point Live Blog From Goldman HQ Is A Wrap – for now…

That’s a wrap for now. But I’ll come back and add a few notes I didn’t get a chance to add today, so come back and check!